Emerging Markets, With or Without China

Over the last few years, a slowing economy and heightened geopolitical risk in China has increasingly led investors to consider dividing their EM allocations into China and ex-China strategies, and we are often asked for our view on removing or reducing China exposure within the Emerging Markets investment universe.

David Oh and Leona Yang, CFA

Over the last few years, a slowing economy and heightened geopolitical risk in China has increasingly led investors to consider dividing their EM allocations into China and ex-China strategies, and we are often asked for our view on removing or reducing China exposure within the Emerging Markets investment universe.

As fundamental stock pickers, we look for quality growth companies that meet our investment criteria. These companies should generate organic top-line growth significantly exceeding GDP growth and, with optimal business models, translate this into even stronger profit growth. When evaluating opportunities within the EM Small Cap universe, we also consider the larger regional or country-specific economic backdrop in which the company operates to enhance our understanding of the associated risks and opportunities. Our analysis includes historical and forecasted GDP growth ranges, as well as valuation, volatility, FX dynamics and other company and country specific factors.

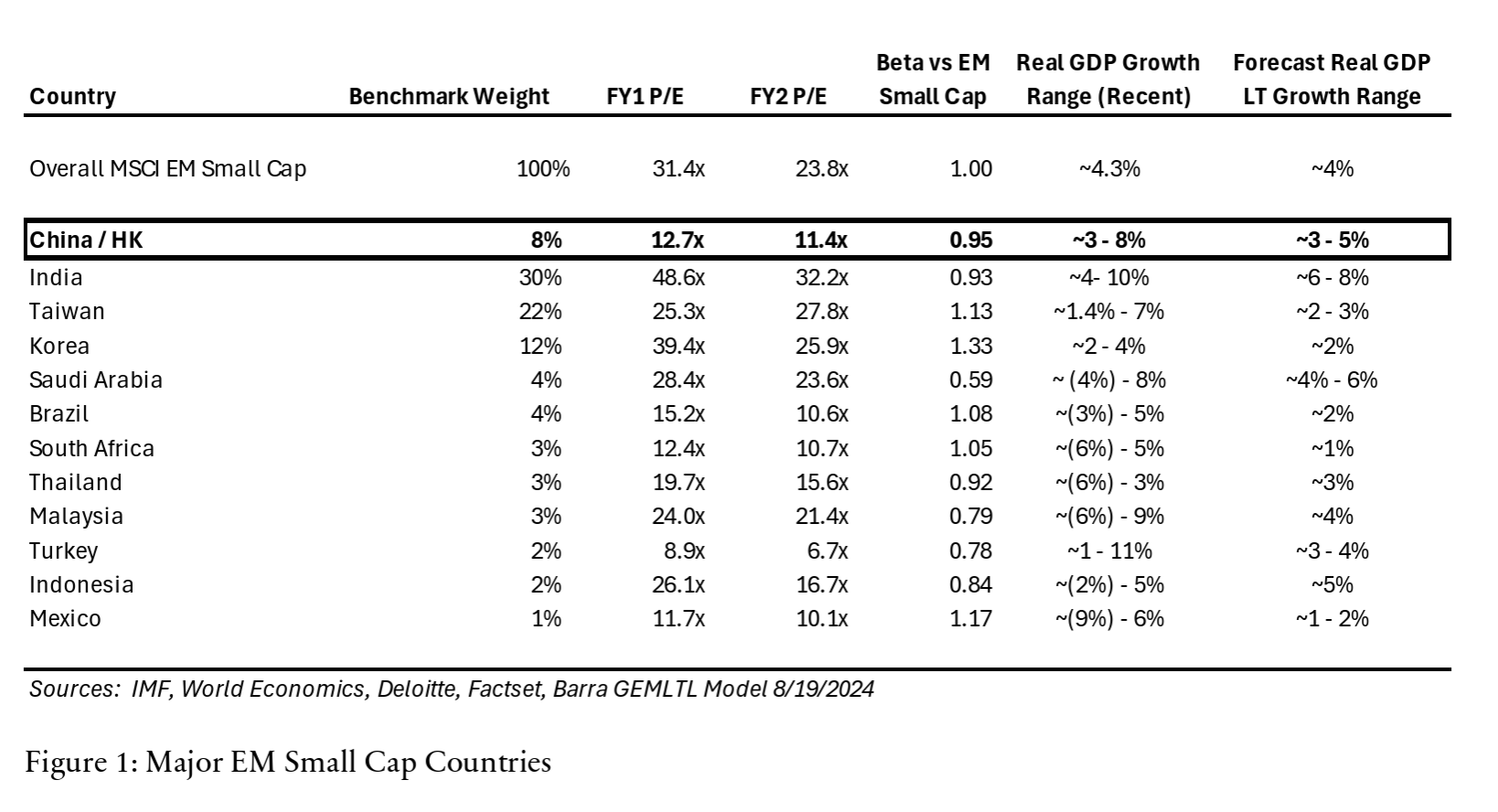

In Figure 1, we summarized GDP growth data (recent and forecasted), country-level valuation and volatility, and benchmark weights for most of the major EM small cap countries, which helps frame our thought process in terms of short-term and longer term returns and risks associated with these markets.

Our Outlook for China

First Quarter 2025 GDP growth expectations are within the 3-5% range as the Chinese government prioritizes higher quality, more sustainable growth, even with its most recent stimulus measures. Against this backdrop, we expect the strongest growth to come from parts of the technology sector including software, healthcare (driven by localization policies and an aging population), and consumerrelated sectors that benefit from both local brand strength and downtrading. Within these sectors, we typically target companies that can sustainably grow their top line by at least 1.5x to 2x GDP, with resulting earnings that should be in the low to mid double digits.

We see opportunities in Chinese companies that have the capabilities to expand abroad, where addressable markets offer higher growth as well as higher margins. These companies, having survived intense competition at home, have developed “lean and mean” capabilities to thrive internationally. In our meetings with Chinese and global companies, we have observed that many Chinese companies are already market leaders not just in China but also globally.

In the current environment, we do not assume significant longer term valuation multiple re-rating, which means our assumed returns are mostly linked to earnings growth and capital returns. There is also potential for downside depending on any further deterioration in US-China relations and capital outflows if investors continue to decrease allocations to China. However, we would note that valuations are quite reasonable, and expectations are low. In the event that economic growth and sentiment improve, there could be substantial upside to earnings growth forecasts and valuation multiples.

Our Outlook for EM ex-China

We anticipate high benchmark weight markets such as India, the aggregated ASEAN (Association of Southeast Asian Nations), and Middle East contributing to strong GDP growth in the near and longer term. These markets benefit from factors driving past EM growth, such as expanding middle-class consumption, infrastructure investment, and supportive government policies. Additionally, they attract capital investment coming from either Chinese or multinational companies re-allocating investment away from China. We believe these trends will persist for the long-term, sustaining these higher GDP growth levels and creating a wealth of investment opportunities with substantial and durable top- and bottom-line growth potential.

For example, while valuations seem elevated in India, we have been able to find companies with strong growth prospects that result in more reasonable long-term valuations. The country’s pro-growth government and a supportive capital market bolstered by the increasing popularity of domestic retail-driven SIPs (systematic investment programs, which are similar to a 401k-style program) since 2017, have also contributed to a favorable investment environment.

Meanwhile, markets such as Taiwan and Korea have more muted GDP growth prospects. Yet, in certain sectors (such as those with companies benefiting from AI investment), we see an ability to achieve above average top and bottom-line growth in the near term. Additionally, Korea and Taiwan engage in high value trading with the entire world, including China and the US. However, we believe that Taiwan and Korea will revert to lower growth in the longer term due to the cyclicality of the IT hardware spending cycle and other export industries that they participate in.

Valuations and expectations for many of these larger benchmark weight markets are elevated, leading us to be more selective about companies from this universe. We would note that China presents a significant opportunity for companies in these other markets in various ways, allowing EM investors to benefit from China exposure even if they are not directly investing in Chinese equities. In any case, an understanding of China and the companies that are pushing into these other markets remains an essential part of any emerging markets strategy.

Emerging Markets Small Cap, with or without China First Quarter 2025

Finally, while Emerging Markets Small Cap has been perceived as a risky asset class, to date the EM Small Cap index has demonstrated a comparable risk profile to the S&P 500 and the EAFE Small Cap indices1.

Meanwhile, Emerging Markets as a whole (with or without China) offers significantly higher GDP growth than developed markets. According to the IMF, EM countries are projected to grow ~4% as compared to developed markets’ GDP growth of ~1.5%. This top-down view is supported by our firsthand experience in these markets, particularly for small cap companies, where we see ambitious entrepreneurs and management teams creating successful businesses, moving fast to capture opportunities, and becoming market leaders by using the latest technologies and lessons learned from analogous companies in other countries.

Regardless of whether investors allocate to China or not, China cannot be ignored. The recent impact of DeepSeek highlights that China is home to engineering talent that is globally competitive and has moved up the value chain.

1 Predicted volatility, Barra GEMLTL Model

This material is for your private information and is provided for educational purposes only. The views expressed are the views of TimesSquare Capital Management, LLC only through the period ending January 2025 and are subject to change based on market and other conditions. The opinions expressed may differ from those with different investment philosophies. The information we provide does not constitute investment advice and it should not be relied on as such. It should not be considered an offer or solicitation to buy or an offer to sell a security. It does not consider any investor’s particular investment objectives, strategies, tax status or investment horizon. We encourage you to consult your tax or financial advisor. All material has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy of, nor liability for, decisions based on such information.

TimesSquare Capital Management LLC is a growth equity specialist that is registered as an investment adviser with the U.S. Securities and Exchange Commission and is majority owned by Affiliated Managers Group, Inc. With an experienced investment team and rigorous fundamental analysis, we identify high quality companies with strong management in inefficient market cap ranges. As a boutique, our highly collaborative process and integrated approach promote our commitment to meeting our clients’ service needs. Importantly, employees share a common economic interest through equity participation, aligning them with the success of our clients and the firm.

TimesSquare Capital Management, LLC

75 Rockefeller Plaza, 30th Floor, New York, NY 10019

©Copyright 2025 TimesSquare Capital Management, LLC. All rights reserved.

This document may not be reproduced, in whole or in part, without permission of the author.

(Blue%20%26%20Gold)(Transparent)(2125x844)%20PNG.png)