February 2026 Newsletter

During the fourth quarter of 2025, TimesSquare proudly celebrated 25 years of Quality Growth Investing. Throughout this time, we have stayed committed to our core investment philosophy while continuously learning, improving, and evolving as a firm.

Firm Updates

Celebrating 25 Years of Quality Growth Investing

During the fourth quarter of 2025, TimesSquare proudly celebrated 25 years of Quality Growth Investing. Throughout this time, we have stayed committed to our core investment philosophy while continuously learning, improving, and evolving as a firm.

"When TimesSquare was founded more than 25 years ago, we had a simple but powerful mission: to build a firm devoted to quality-growth investing with a distinctive focus on small- to midcap equities. That clarity of purpose has guided us through market cycles, allowing us to uncover opportunities often overlooked by the market. I am incredibly proud of the results this commitment has delivered for our clients, and I’m inspired by the potential that lies ahead as we continue to pursue excellence over the next 25 years and beyond.”

- Grant Babyak, CEO

New Vehicle Launch TSCM:

TimesSquare Quality Mid Cap Growth ETF This product leverages TimesSquare’s 25-year investment history of creating quality growth portfolios into a taxefficient and transparent ETF structure. We believe TSCM fills the necessary gap of actively managed mid cap growth ETFs being offered in today’s marketplace.

Read the full Press Release here.

2025 Annual Portfolio Manager Letters

Executive Summary

In 2025, we continued to strengthen our investment platform through internal promotions and the addition of investment talent to reinforce the depth, continuity, and expertise of our team. Developing talent from within and a continued focus on enhancing our research capabilities remain central to TimesSquare’s long-term success.

Across strategies, our rigorous bottom-up research was reflected in high conviction quality growth investments in our respective strategies. U.S. Mid Cap Growth delivered strong relative performance, U.S. Small Cap Growth remained disciplined in a factor-driven market, and International Small Cap Growth capitalized on structural themes despite geopolitical and style headwinds.

As we enter 2026, we believe markets will increasingly reward selectivity over broad exposure. With reshoring, defense modernization, and AI infrastructure now structural forces, we remain focused on identifying durable businesses, backing disciplined management teams, and acting decisively as facts evolve.

Research Analyst Deep Dive – Core Industrial Themes

The image of Industrials as a slow-moving, legacy asset class is a relic of the past. Driven by a surge in AI capital spending and a renewed appreciation for low obsolescence risk, the sector has moved from the sidelines to the spotlight. This edition of Research Analyst Deep Dive explores the fundamental strength of modern Industrials and the forces that are coming together to drive a bright future for the sector in an AI-powered physical world.

Sector Outlook

We believe the Industrials sector is entering a healthier period, underscored by broadening growth and short-cycle volume recovery. Several trends support this view:

- Manufacturing PMI emerging from contraction. The ISM Manufacturing PMI is emerging from a prolonged period of contraction, corroborating the well-established relationship with Fed easing. When paired with low channel inventories, this is a recipe for a classic cyclical rebound.

- AI capital investment providing a multi-year runway. Capital investment related to AI is driving growth across an array of industrial products and services within this ecosystem.

- Defense budget tailwinds. Escalating geopolitical tensions, the potential for an outsized defense budget, and a generational shift in the Pentagon’s spending priorities are driving robust growth across well-positioned small- and mid-cap defense technology companies.

- Commercial aerospace OEMs ramping production. Production is broadening following years of supply chain disruption and quality control shortfalls.

While stock prices may remain volatile in the short term, underlying demand for many industrial businesses appears steady and/or improving. While we’ve seen a strong appetite for cyclical stocks early in the year, the earnings torque embedded in many of these businesses can support continued upside, in our view.

Cyclical Reacceleration

The ISM Manufacturing PMI spent the last three years essentially in contractionary territory—one of the longest stretches of manufacturing weakness in decades. This has been a significant headwind for the general industrial complex. For months, investors have been awaiting an inflection given the historical linkages between monetary easing and PMI expansions. Headline data was generally uninspiring until recently.

The January 2026 PMI reading marked a key development, coming in at 52.6 (>50 indicates growth) and surging nearly five points from December’s 47.9. That was the first expansionary reading in 12 months and marked the highest level since 2022. Moreover, the leading indicator within this index—new orders—jumped to 57.1, the strongest level since early 2022. Additionally, the February report exhibited decent follow-through with the overall index remaining at 52.4 and new orders remaining at a strong 55.8. We shouldn't declare victory yet; the recent SCOTUS tariff ruling and the energy shock following the joint attack on Iran have introduced fresh uncertainty. However, the underlying headline data is undeniably positive, and it’s validated by improving order activity at key short-cycle bellwethers.

Outlook: Short-cycle management teams have been reluctant to extrapolate a solid start to the year within their outlooks, which sets the table for outperformance should industrial reacceleration continue. We largely focus our short-cycle exposures on companies poised to benefit from a blend of secular and cyclical drivers, reducing risk in the event of cyclical retrenchment. A looming risk for short-cycle industrials is how companies react to the recent SCOTUS IEEPA tariff decision and the subsequent 15% global tariff implemented under Section 122 of the Trade Act of 1974. Another important watch item is the upcoming joint review of the USMCA trade pact in July. However, with midterm elections approaching, we see pressure on the administration to work quickly toward tariff clarity to avoid stalling the cyclical recovery that is already underway.

Commercial Aerospace: Growth Handoff from Aftermarket to OEM

The commercial aircraft production cycle remains in its early innings, decoupled from its historically late-cycle roots due to numerous factors that have constrained the aircraft production recovery for multiple years. Production ramps at key OEMs are supported by multi-year backlogs, easing regulatory pressure on Boeing, and ongoing supply chain normalization.

An aging and highly utilized aircraft fleet has supported several years of outstanding growth in aftermarket parts demand. With valuations elevated coming into the year and aftermarket growth decelerating—albeit from very attractive rates—we see a more attractive risk/reward profile at OEM-focused aerospace suppliers.

Outlook: We see commercial aircraft builds eclipsing the prior peak (2019) by over 35% by the end of the decade. We seek exposure to OEM suppliers leveraged to the programs with the greatest relative upside to full production, as well as companies in advantageous market positions that should capture outsized pricing as demand for long-lead-time components and materials threatens to outstrip supply in future years.

AI Capex: Multi-Year Structural Tailwind

The unprecedented magnitude of the AI capex boom has created a far-reaching stimulus that is stretching well beyond the compute value chain and has buoyed numerous areas within the industrials sector. The 65%+ year-over-year capex growth forecast across the “Big Five” hyperscalers for 2026—paired with a shift to higher-performance compute and enabling technologies—is driving robust demand for thermal management, electrical and power generation equipment, as well as the specialty contracting services that integrate and install these critical systems at data centers.

Lengthy interconnection queues and a speed-to-market focus underpinning AI capex plans have shifted the power generation conversation toward behind-the-meter applications, whereas a year ago, the focus was largely on large power purchase agreements between hyperscalers and independent power producers. With heavy-frame gas turbine lead times stretching past four years, hyperscalers are increasingly embracing configurations that will rely on fuel cells, mobile gas turbines, reciprocating engines, and aeroderivative turbines to solve the time-to-power problem inherent in rapid data center deployment.

We have a preference in the portfolio for specialty contractors given: (1) the relative valuation discount versus AI capex component suppliers despite similar growth rates; (2) underappreciated pricing leverage enabled by the scarcity of skilled trade labor; and (3) in the unexpected event of a slowdown in AI capex, contractors that can shed labor with relative ease would fare disproportionately better than manufacturers facing overcapacity.

Outlook: The AI capex complex has a multi-year runway of growth ahead of it. Breakneck demand for critical systems within data centers is driving outsized growth at suppliers with the ability to offer customizable critical systems solutions with relatively attractive lead times. As data center technologies evolve and lead times normalize, we expect to see differentiated performance among equipment suppliers with global scale and best-of-breed solutions capable of keeping pace with the technical roadmap, enabling next-generation compute. Should an AI bellwether alter its technical roadmap in a meaningful way, we see the lowest risk of creative destruction within the specialty contractors.

Defense: Policy Tailwind Building

The Trump administration has voiced a strong intent to make generational investments in the U.S. military’s arsenal and warfighting capabilities. Simultaneously, EU NATO Allies are taking their security far more seriously, with defense spending ramping from roughly 1.5% of GDP over the prior decade to a 5% target by 2035. Both forces are combining to support an exceptional era of demand for allied defense contractors and suppliers. Additionally, a sizeable reconciliation bill could dramatically expand the U.S. defense budget, creating a very favorable backdrop for companies serving the highest-priority areas within the military. Areas such as hypersonic weapons, Golden Dome, military space and satellite infrastructure, unmanned and counter-unmanned systems, submarines, and restocking of strategic and tactical missiles are all poised to benefit. Additionally, the principles laid out in Secretary Hegseth’s “Arsenal of Freedom” speech support recapitalizing the small- and mid-cap military industrial complex—a deliberate shift away from relying on a handful of large defense primes for the majority of the military’s needs. Importantly, this view has been substantiated by a strong pace of new contract wins at smaller prime contractors in recent quarters.

Outlook: We see an attractive opportunity for small- and mid-cap defense technology companies to capture an increasing share of a growing defense budget as the Pentagon shifts budget priorities away from expensive legacy programs toward asymmetric warfare, next-generation deterrents, and achieving superiority in new domains. We focus on defense technology suppliers with affordable, de-risked solutions that shorten time-to-combat and stand out as more attractive options than expensive, built-to-suit offerings at traditional prime contractors with lengthier deployment timelines.

Bottom Line

We believe the industrial sector is ripe with trends that remain in the early innings of growth, particularly around a broader short-cycle industrial reacceleration, ramping commercial aircraft production, rising defense technology demand, and rapid AI data center deployment. Despite the recent outperformance of the sector, we see favorable risk/reward in Industrials relative to other sectors that face greater vulnerability to structural debates around AI disintermediation, potential government policy headwinds, and consumer affordability issues.

2025 Annual Portfolio Manager Letters

U.S. Mid Cap Growth, U.S. Small Cap Growth, & International Small Cap Growth

As we reflect on another year, we would like to start by expressing our appreciation for the trust you have placed in us to manage your investments. We recognize that this responsibility represents a meaningful partnership, and we approach it with a strong sense of accountability and a long-term perspective. Our focus remains on thoughtful capital stewardship, disciplined execution, and alignment with our clients' long-term goals.

The Strength of Our Bench

Our success is a direct result of the talent we foster. We are proud to announce the promotions of Ed Salib and Greg Vasse to Portfolio Manager. Ed, who began as our first intern in 2000, and Greg, who joined the firm as an Associate in 2009, have each earned their respective PM roles through years of dedication, performance, and investment excellence, embodying the culture of longevity and deep institutional knowledge we prize at TimesSquare. We are also pleased to recognize David Hirsh’s promotion last year to Co-Head of the International Team.

Together, these leadership advancements reflect our longstanding commitment to developing talent from within and underscore the depth, continuity, and global expertise of our investment team. We believe these qualities form the foundation of our success and position us strongly for the future.

We’ve also strengthened our research platform with the promotions of Jacob Troutman and Margot Waldron from Associate to Analyst—reflecting their expanding analytical responsibility, deepening sector expertise, and increasing ownership across our Financial Technology, Business Services, & Energy, and Health Care coverage, respectively.

In addition, we are pleased to welcome Adam Krasner (Analyst: Financials) and Ryan Williams (Associate), further enhancing the breadth and depth of our team. This year, we intend to continue bolstering our research efforts with a focus on finding talented individuals to support Health Care and Information Technology.

We aren’t just managing a portfolio; we are building a multi-generational engine of research.

2026 Outlook: A Stock-Picker’s Market

We are entering a year where "easy beta" is a thing of the past. The narratives of 2025 — reshoring, energy independence, and security - are now the baseline. We are closely watching the Supreme Court’s stance on the “Liberation Day” tariffs. Regardless of the legal outcome, the protectionist intent is here to stay. In this environment, we aren't looking for "macro winners"; we are looking for the companies providing the "picks and shovels" for this new era. We remain enthusiastic about the opportunities this environment presents, and the ideas currently represented in the portfolio, and we look forward to navigating the evolving market landscape in partnership with you.

U.S. Mid Cap Growth

Portfolio Manager & Analyst

Portfolio Manager

Portfolio Manager & Analyst

2025 Recap: High Conviction in Execution

Throughout 2025, the team remained steadfast in our process — conducting over 1,500 management meetings and implementing 24 new ideas - ensuring every action reflected our disciplined approach to portfolio construction. The U.S. Mid Cap Growth portfolio returned 10.2% (gross) and 9.4% (net), outperforming Russell Mid Cap Growth’s 8.7% return for the full year.

Our performance was driven by identifying companies that turned macro headwinds into competitive moats:

- The AI Pivot: We’ve moved past the "hype" phase. We took gains in AppLovin (+100% in 2025) as it exited the benchmark and eventually the portfolio (due to its size). Meanwhile, we remain high on JFrog, which proved its mission-critical status after a major global supply chain attack.

- National Infrastructure: As the U.S. shifts toward a $1 trillion defense budget and AI-driven data centers, we focused on "high-moat" providers like Curtiss-Wright and EMCOR. These aren't just industrial stocks; they are the backbone of national security and digital infrastructure.

- Navigating Challenges: Not every thesis plays out perfectly. In Inspire Medical, we saw operational missteps and a DOJ inquiry that breached our standards for execution. We exited the position decisively. Part of stewardship is knowing when the facts have changed and acting without sentimentality.

U.S. Small Cap Growth

Portfolio Manager & Analyst

Portfolio Manager

Portfolio Manager & Analyst

Navigating a Challenging 2025

Throughout 2025, the team remained steadfast in our process — conducting over 1,500 management meetings and implementing 34 new ideas - ensuring every action reflected our disciplined approach to portfolio construction. The U.S. Small Cap Growth portfolio returned 6.9% (gross) and 5.9% (net) for the year. While positive, this trailed the Russell 2000 Growth Index’s 13.0% return.

It is important to be candid about why: for much of the third quarter, the market favored "low-quality" factors. Specifically, companies with zero or negative earnings and high-volatility profiles. As a firm rooted in fundamental discipline, we do not chase momentum for momentum’s sake. While this cost us relative performance in the short term, we saw these extremes begin to rotate in the fourth quarter. The adjustments we made during a volatile third quarter enabled us to finish the year with renewed momentum in both the Industrials and Technology sectors.

Conviction in Action: Sector Insights

Health Care - Cashing in on Innovation: Our strategy in Health Care remains focused on novel therapies that command premium pricing. 2025 was a year of "monetizing" our winners. We saw three of our holdings, Intra-Cellular, Verona, and Merus, go through successful acquisitions. Furthermore, Insmed performed so well that it "graduated" from our Small Cap universe to our Mid Cap strategy. However, we also showed discipline in exiting Inspire Medical Systems. When operational missteps and inventory issues clouded the thesis, we moved on. Conversely, we used the temporary weakness in Vericel to increase our position; our patience was rewarded as procedure volumes rebounded late in the year.

Industrials - The Defense and Infrastructure Tailwinds: We have strategically invested in the broader shift toward defense modernization. Kratos Defense was a standout, gaining 203% during the period, on the back of massive unmanned systems contracts. We managed this position actively, trimming on strength and adding on dips to maintain optimal sizing. While we exited ACV Auctions as economic headwinds hampered their digital marketplace, we saw a "graduation" success story in Comfort Systems, which we moved to our Mid Cap strategy after an 86% run driven by data center and semiconductor demand.

Technology - Beyond the AI Hype: The "AI eats Software" narrative created significant volatility this year. We focused on the "show-me-the-money" winners like JFrog, which surged 112% in 2025, thanks to a mission-critical win with OpenAI and its essential security role following a major supply chain attack. We parted ways with PAR Technology when the implementation of new contracts fell short of our expectations. Regarding Vertex, while the stock retrenched, we believe the business is now significantly de-risked and are monitoring its ability to execute in early 2026.

International Small Cap Growth

Portfolio Manager & Analyst

Portfolio Manager & Analyst

2025 Recap: High Conviction in Execution

We are particularly proud of what the team accomplished in 2025: visiting 17 countries, participating in over 600 research meetings, and implementing 27 new ideas into our portfolio. Despite headwinds from factors consistent with our investment style — positive exposure to Profitability and negative exposure to Book-to-Price & Dividend Yield – our 2025 performance was not a product of following the crowd but maintaining discipline when markets turned "low-quality."

Europe | Sovereignty & Re-Industrialization: Beyond energy and defense, Europe’s mandate now encompasses technological sovereignty, fueling a cyclical recovery in IT services ahead of 2026 spending packages. We proactively trimmed defense holdings on valuation early in the year, later using geopolitical volatility to rebuild exposure in mission-critical leaders like RENK as visibility extended toward 2030.

Japan | The “Takaichi Trade” & Structural Shifts: After capitalizing on record inbound tourism and robust domestic spending, we pivoted away from consumer-facing names, such as Food and Life on valuation and ABC-Mart, following a reassessment of inbound demand and ongoing challenges in its Korean business. Instead, we increased allocation into structural growth engines with the Takaichi administration’s strong support for energy independence and technology advancement. As a result, throughout the year, we built positions in grid-related names such as SWCC.

Asia/Pacific ex-Japan | Resource Security: A chronic deficit in critical minerals, combined with heightened geopolitical friction, has altered regional mining dynamics. National security considerations now outweigh traditional project economics in many countries, reshaping capital flows in the mining sector. This has benefited mining technology and infrastructure providers, supporting performance in ALS and IMDEX.

Emerging Markets | Tariff and AI: Earlier in the year, emerging markets with significant technology and export exposure faced pressure from proposed U.S. tariffs and the release of DeepSeek, which raised questions around global AI infrastructure spending. Sentiment improved as the administration signaled greater flexibility on trade and global hyperscalers reaffirmed long-term AI investment plans.

2026 International Outlook:

The conflict in the Middle East has caused Equity markets to shift abruptly from a "Goldilocks" scenario (sustained growth/low inflation) to concerns about potential stagflation, driven by lower growth and energy-cost-induced inflation that limits central banks’ ability to accommodate. While these events create headlines and heightened volatility, we believe investors are reacting to short-term uncertainty rather than a shift in long-term fundamentals. Prior to this period of geopolitical tension, February data confirmed a bullish macro backdrop: rising growth, falling inflation, and declining rates.

Given the fluid situation, we are avoiding aggressive portfolio changes and remain constructive on International Equities over the medium term:

- Global PMIs are improving, and fiscal expansion in economies like Germany is beginning to materialize.

- The improving macro environment supports a potential growth inflection point outside the U.S.

- Although energy-dependent regions such as Europe and Asia may seem vulnerable in the short term, if the Iran situation remains contained, markets will likely refocus on the significant valuation discount between non-U.S. and U.S. equities.

While geopolitical fragmentation and shifting trade frameworks create headlines and short-term volatility, they also create the very dislocations where our fundamental, bottom-up approach thrives. As the global landscape continues to reorder around resilience and security, we remain committed to our core philosophy: identifying steady, disciplined management teams capable of compounding value regardless of macroeconomic noise. The current environment is complex, but for a nimble team with deep fundamental and geographic expertise, complexity is an opportunity. We are excited about the ideas currently in our portfolio and look forward to navigating this evolving landscape alongside you.

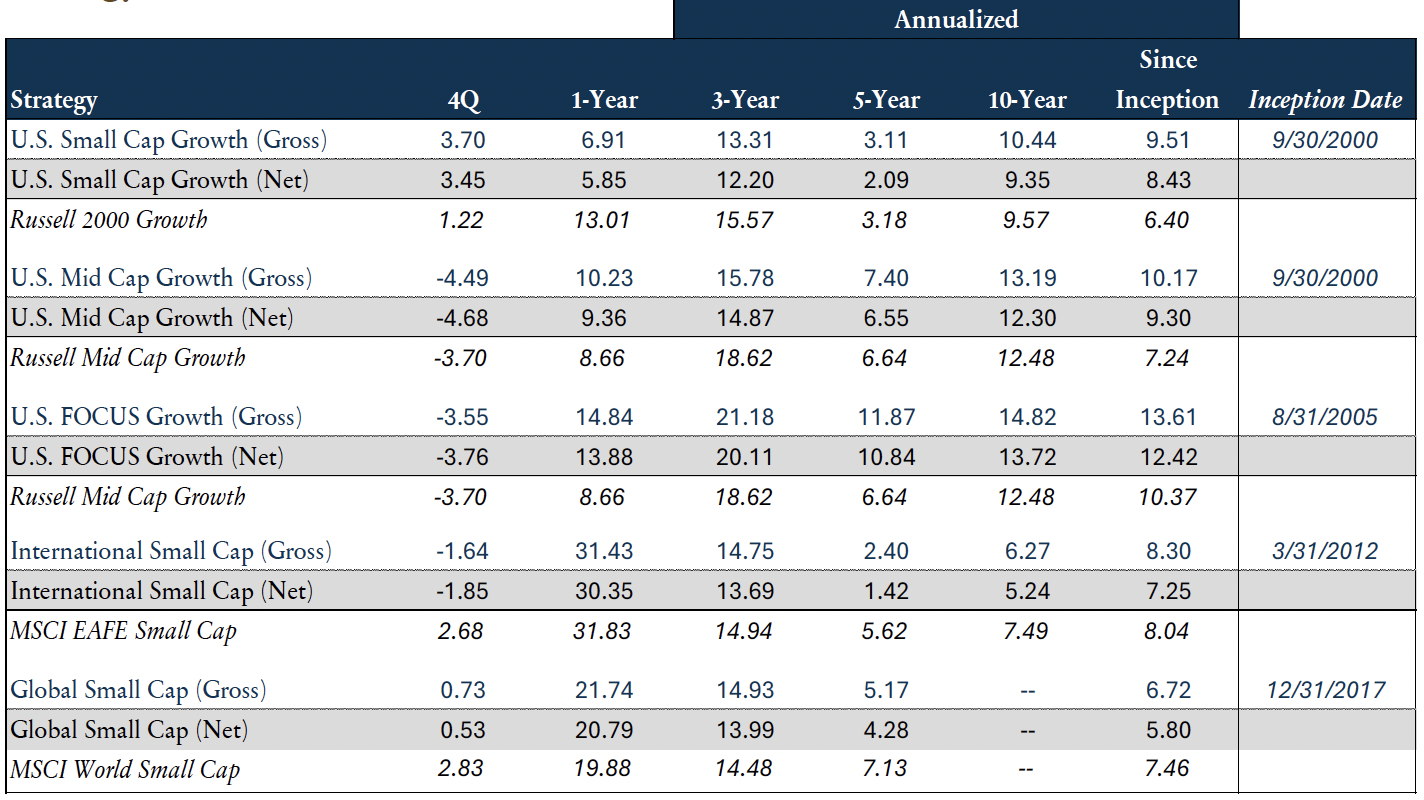

Strategy Performance

Please see important disclosures on pages 8-9.

Past performance does not guarantee future results. There is risk that invested capital may be lost.

Updated Profiles & Commentaries Here

TimesSquare News & Insights

TimesSquare Announces the Launch of the TimesSquare Quality Mid Cap Growth ETF (TSCM)

We’re proud to share that the 𝐓𝐢𝐦𝐞𝐬𝐒𝐪𝐮𝐚𝐫𝐞 𝐐𝐮𝐚𝐥𝐢t𝐭𝐲 𝐌i𝐝 𝐂𝐚𝐩 𝐆𝐫𝐨𝐰𝐭𝐡 𝐄𝐓𝐅 (Nasdaq: 𝐓𝐒𝐂𝐌) has surpassed $𝟐𝟐𝟓 𝐦𝐢𝐥𝐥𝐢𝐨𝐧 in assets (as of 2/11/26), marking an important early milestone for the fund.

AI & the Durability Debate

Finding Quality in the SaaSacre: Evaluating how artificial intelligence is redrawing competitive boundaries in enterprise software, pressuring traditional seat-based models, and challenging long-held assumptions around pricing power and terminal value.

Inside the Investment Room (January 2026)

This inaugural edition of Inside the Investment Room pulls back the curtain on how TimesSquare invests when macro forces and fundamentals intersect. Grounded in disciplined bottom-up research and sharpened by macro awareness, it explores the crosscurrents shaping capital allocation, valuation, and risk across sectors, from rates and inflation to AI and evolving market breadth. It is a candid look at how ideas are pressure-tested, where opportunity is emerging, and why conviction still starts at the company level.

HedgeFundAlpha Interview with Sonu Chawla, CFA, Portfolio Manager

Sonu Chawla brings nearly two decades of experience as a disciplined quality growth investor, with a strong emphasis on fundamental research, management quality, and long-term compounding. Her investment philosophy, “growth with a conscience,” guides TimesSquare’s differentiated approach to mid-cap equities, positioning the firm to generate alpha across market cycles.

Disclosures

TimesSquare Capital Management LLC is a growth equity specialist that is registered as an investment adviser with the U.S. Securities and Exchange Commission and is majority owned by Affiliated Managers Group, Inc. With an experienced investment team and rigorous fundamental analysis, we identify high quality companies with strong management in inefficient market cap ranges. As a boutique, our highly collaborative process and integrated approach promote our commitment to meeting our clients’ service needs. Importantly, employees share a common economic interest through equity participation aligning them with the success of our clients and the firm.

This material is for your private information and is provided for educational purposes only. The views expressed are the views of TimesSquare Capital Management, LLC only through the period ended February 2026 and are subject to change based on market and other conditions. The opinions expressed may differ from those with different investment philosophies. The information we provide does not constitute investment advice and it should not be relied on as such. It should not be considered an offer or solicitation to buy or an offer to sell a security. It does not consider any investor’s particular investment objectives, strategies, tax status or investment horizon. We encourage you to consult your tax or financial advisor. All material has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy of, nor liability for, decisions based on such information. Specific investments described herein do not represent all investment decisions made by TimesSquare. No assumption should be made that investment decisions identified and discussed were or will be profitable. Specific investment advice references provided herein are for illustrative purposes only and are not necessarily representative of investments that will be made in the future.

TimesSquare Capital Management, LLC claims compliance with the Global Investment Performance Standards (GIPS®) and is independently verified. A firm that claims compliance with the GIPS standards must establish policies and procedures for complying with all the applicable requirements of the GIPS standards. Verification provides assurance on whether the firm's policies and procedures related to composite and pooled fund maintenance, as well as the calculation, presentation, and distribution of performance, have been designed in compliance with the GIPS standards and have been implemented on a firm-wide basis. Policies for valuing investments, calculating performance, and preparing GIPS Reports are available upon request. GIPS® is a registered trademark of CFA Institute. CFA Institute does not endorse or promote this organization, nor does it warrant the accuracy or quality of the content contained herein.

Certain information contained herein has been obtained from third party sources and such information has not been independently verified by TSCM. No representation, warranty, or undertaking, expressed or implied, is given to the accuracy or completeness of such information by TSCM or any other person. While such sources are believed to be reliable, TimesSquare does not assume any responsibility for the accuracy or completeness of such information. It does not undertake any obligation to update the information contained herein as of any future date.

Any indices and other financial benchmarks shown are provided for illustrative purposes only, are unmanaged, reflect reinvestment of income and dividends and do not reflect the impact of advisory fees. Investors cannot invest directly in an index. Comparisons to indexes have limitations because indexes have volatility and other material characteristics that may differ from a particular hedge fund. For example, a hedge fund may typically hold substantially fewer securities than are contained in an index.

Certain information contained herein constitutes “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results or actual performance may differ materially from those reflected or contemplated in such forward-looking statements. Nothing contained herein may be relied upon as a guarantee, promise, assurance or a representation as to the future.

U.S. Small Cap Growth: Performance is measured against the Russell 2000® Growth – a market capitalization-weighted index that measures the performance of those Russell 2000® companies with higher price-to-book ratios and higher forecasted growth rates. All indexes, including the Russell 2000® Growth Index, are based on gross-of-fee returns. FTSE Russell is the source and owner of the Russell Index data contained or reflected in this material and all trademarks and copyrights related thereto. Benchmark returns are not covered by the report of independent verifiers.

U.S. Mid Cap Growth: Performance is measured against the Russell Midcap® Growth – a market capitalization-weighted index that measures the performance of those Russell Midcap® companies with higher price-to-book ratios and higher forecasted growth rates. All indexes, including the Russell Midcap® Growth Index, are based on gross-of-fee returns. FTSE Russell is the source and owner of the Russell Index data contained or reflected in this material and all trademarks and copyrights related thereto. Benchmark returns are not covered by the report of independent verifiers.

The performance figures shown for U.S. Small Cap Growth and U.S. Mid Cap Growth are calculated in U.S. dollars on a size-weighted basis and reflect the reinvestment of dividends and other earnings, and the deduction of brokerage commissions and other transaction costs. Performance is provided on a gross basis (before the deduction of management fees) as well as net of the highest fee level from the standard fee schedule listed for this strategy during the period presented. The U.S. Small Cap Growth fee basis is 100 basis points, and the U.S. Mid Cap Growth fee basis is 80 basis points. Investment advisory fees generally charged by TimesSquare are described in Part 2A of its Form ADV.

(Blue%20%26%20Gold)(Transparent)(2125x844)%20PNG.png)