May 2025 Newsletter

TimesSquare reached a milestone anniversary celebrating its 20-year partnership with Affiliated Managers Group, Inc. (AMG) as an independent affiliate.

Firm Updates

TimesSquare reached a milestone anniversary celebrating its 20-year partnership with Affiliated Managers Group, Inc. (AMG) as an independent affiliate.

Personnel Updates

We thank Michael Russell, U.S. Research Analyst, for his incredible contributions to the firm over the last 19 years. Mike had a wonderful 30-year career in the investment industry, and we wish him all the best in his next chapter. His retirement was effective March 31, 2025.

Notable Updates

U.S. Investment Team – We are currently undergoing the process of evaluating candidates for a Research Associate to join the team.

Why International and Why Now

Executive Summary

- U.S. equities face historically high valuations and economic uncertainty, creating compelling relative value in international markets.

- Europe is positioned for future growth through structural investments for technological sovereignty, energy independence, and defense autonomy.

- In Japan, economic reforms, rising domestic wages, and a surge in foreign tourism are fueling both consumer demand and long-term expansion.

- Small Cap companies in these regions, which are more tightly linked to local economies, offer targeted exposure to domestic growth with less global macro sensitivity.

- A disciplined quality growth approach can help investors navigate uncertainty and capture international opportunities.

Market Overview (1Q 2025)

Expectations for businesses and markets were broadly positive as 2025 began. Hopes for a pro-business, lighter regulatory environment lifted global markets in January. However, delays and uncertainties regarding U.S. policies tempered markets in February and the U.S. pulled back sharply in March.

- In the first quarter, broad-based weakness of U.S. equities (-5% return for the Russell 3000 Index) lagged overseas markets (7% for the MSCI EAFE Index and 3% for the MSCI Emerging Markets Index).

- Even before the market’s tariff tantrum at the start of April, there were inflationary pressures. Global Purchasing Manager Indices (PMIs) showed moderating New Order rates and higher Prices Paid/Output for manufacturing and service activities.

- While value indices outperformed growth, both Growth and Value had positive returns among global risk factors. It was the negative showing from Beta that overwhelmed everything else

Analyst Updates

As our investment teams meet with companies, review recent earnings reports, and survey the global landscape, they note several investment dynamics that inform our positioning:

In Information Technology, reverberations remained from January’s announcement that China’s DeepSeek AI model could produce competitive results at a lower cost.

- Concerns about reductions in the massive spending rates on AI related infrastructure (e.g., data centers) weighed on semiconductors and related industries.

- Among corporate IT buyers, budget surveys pointed to more moderate spending (though with resilience expected for AI and cybersecurity).

Spending slowed for Consumers,

- Creeping inflation was the initial headwind.

- March’s level of U.S. Consumer Confidence also fell to a four-year low.

The U.S. regulatory environment was expected to support more activity among Financial Services companies.

- Corporate America has delayed M&A activity or other large financing projects until there is more clarity regarding the fiscal budget, interest rates, and (most recently) trade policies.

Weakness in PMIs led to pullbacks within the Industrials sector.

- Longer cycle areas or those with high degrees of recurring revenues have held up better.

- Companies that previously expected demand to recover in the second half of 2025, saw their hopes fade.

Why International and Why Now

Magnus Larsson, David Hirsh and Leona Yang, CFA

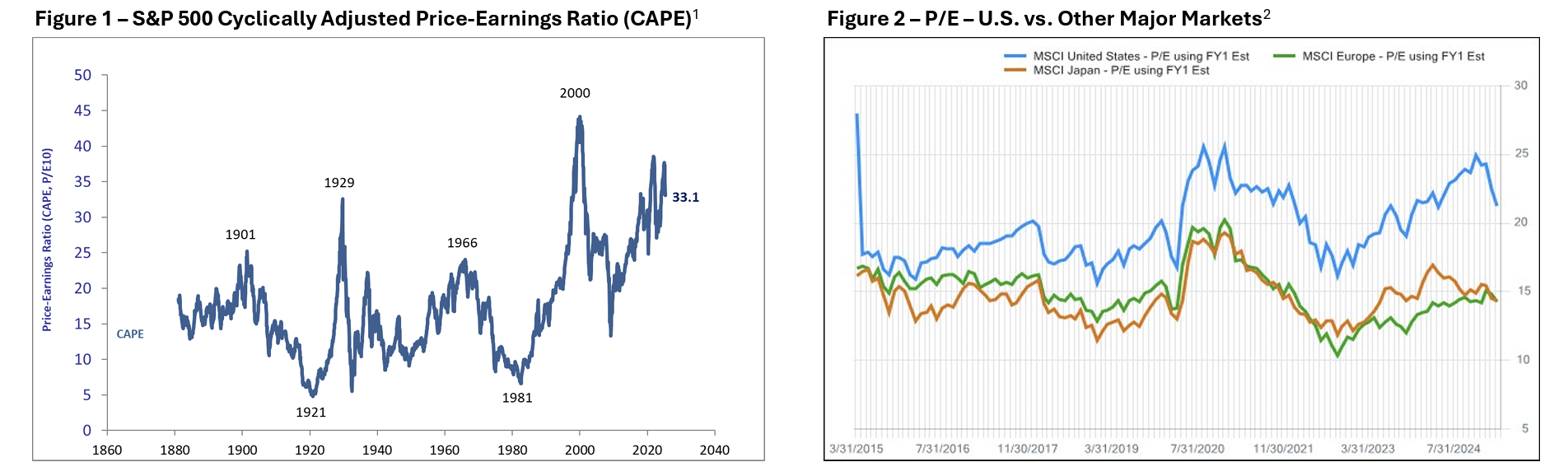

Investors have favored the U.S. equity market for many years. However, with U.S. stocks currently experiencing historically high valuations and an uncertain economic outlook, there is a growing interest to look beyond the domestic markets. We note in the following charts the historically high valuations in the U.S. equity market and the widening of that valuation gap versus other major world markets.

Case Studies – Europe and Japan

As a bottom-up quality growth specialist with decades of experience in international markets, we believe there are compelling opportunities outside the U.S. Below we examine Europe and Japan, the two largest markets within the exU.S. universe.

Europe

A growing awareness across Europe underscores the necessity of decoupling from foreign influences in various sectors. Beyond energy and, more recently, defense independence, current tariff concerns are highlighting the urgency of trade decoupling. Looking ahead, we anticipate a medium-term objective of greater European technological sovereignty, recognizing infrastructure like the cloud as strategic assets. This multifaceted decoupling trend will necessitate significant investment, which in turn will lead to growth within several key sectors of the European economy. Despite short-term headwinds causing lower business and consumer sentiment in Europe, increased reshoring and investments in domestic production provide an attractive backdrop. Furthermore, the historic German stimulus announced in March is the strongest evidence that the EU is up to the challenge and shouldn’t be underestimated in realizing this potential. For this medium-term expansion to materialize, Europe needs updated infrastructure, requiring government spending and lower taxes. The ongoing decline in Eurozone inflation also supports this positive outlook, allowing the European Central Bank to maintain an accommodative policy stance. Consequently, European economic growth should be buoyant in 2026. In the short term, this uncertainty might help the ECB manage inflation. Our approach in the region includes balanced exposure to both local structural growth drivers and global niche dominators.

Japan

After decades of stagnation, Japan is undergoing economic reforms, particularly in terms of corporate governance, labor market participation, and foreign investment. These changes should yield long-term growth.

The demographic reality of an aging population in Japan underscores the urgent need for advancements in technological innovation. To offset potential labor shortages and maintain productivity, the nation is increasingly focused on digitization across various sectors. This is expected to drive significant digital investment, coupled with the strategic implementation 1 Source: Robert Shiller (https://shillerdata.com/), Price earnings ratio is based on average inflation-adjusted earnings from the previous 10 years, known as the Cyclically Adjusted PE Ratio (CAPE Ratio). Data from January 1,1871 to April 3, 2025. 2 Source: FactSet, MSCI, FY1 PE was used for this analysis. 3/31/2015-3/31/2025. 3/7of AI to improve efficiency in industries ranging from manufacturing to services. Against this backdrop, companies that are involved in the development of local data centers, semiconductor foundries, or part of the electric grid ecosystems are poised for substantial long-term growth.

The major expansion of NISA (Nippon Individual Savings Account) in 2024 introduced changes to the system including making the NISA system permanent, the NISA tax-exempt holding period indefinite, and increasing the investment limits. Meanwhile, Japan’s corporate governance reform pushes Japanese companies to improve profitability and to drive future growth. These changes provide a supportive backdrop to Japanese equities.

With tariff worries weighing on export related sectors across the world, our attention is drawn to Japan’s robust inbound tourism. While closely monitoring this influx of international visitors, we also anticipate that the recent significant wage increases within Japan will provide a strong tailwind for domestic spending in the quarters ahead.

Small Caps

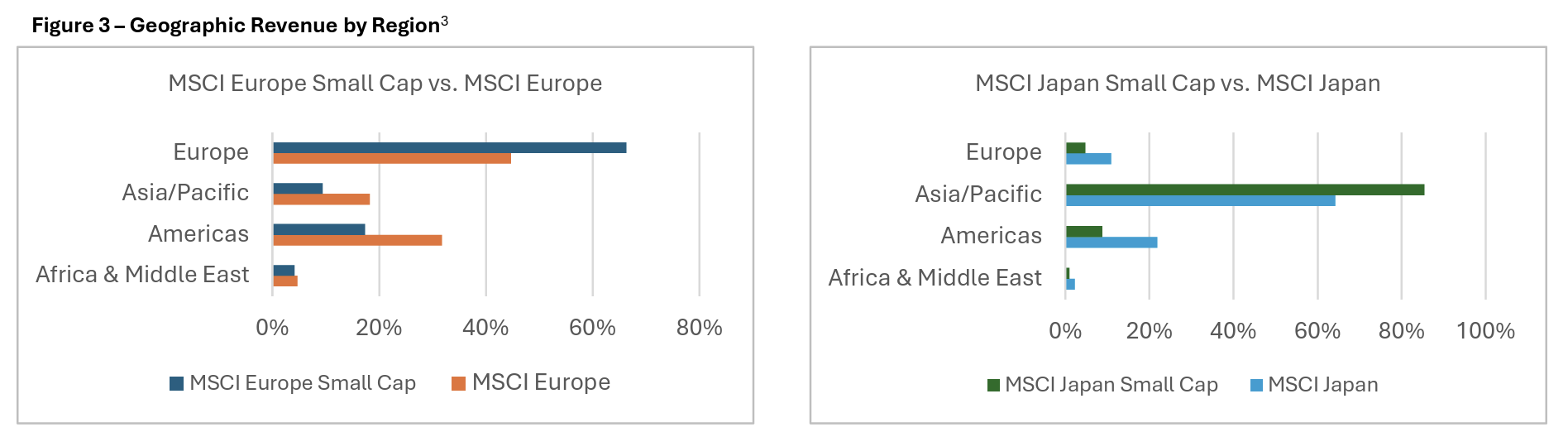

As illustrated in Figure 3, on average, smaller cap companies in Japan and Europe generate higher proportions of their revenues domestically. This ties them more directly to the local economic fundamentals and consumer behaviors. By allocating to small cap companies, investors have the opportunity to gain targeted exposure to local economies and potentially capture idiosyncratic growth opportunities that are less susceptible to global macroeconomic and geopolitical influences.

Why a Quality Growth approach matters?

Investment styles and asset classes may rise and fall in popularity during market cycles due to macroeconomic changes or investment sentiment. As bottom-up investors with a focus on business fundamentals, we seek high quality growth companies with a competitive edge - those with pricing power, strong management teams, and robust balance sheets. These companies, even during turbulent markets, tend to exhibit greater resilience and offer higher visibility in future growth. Given our preference for differentiated companies, we seek to have a positive exposure to profitability and growth highlighting an unwavering commitment to style consistency in our portfolio.

We believe the solidity of this approach will lead to better outcomes for our investors and do so in a risk-managed way.

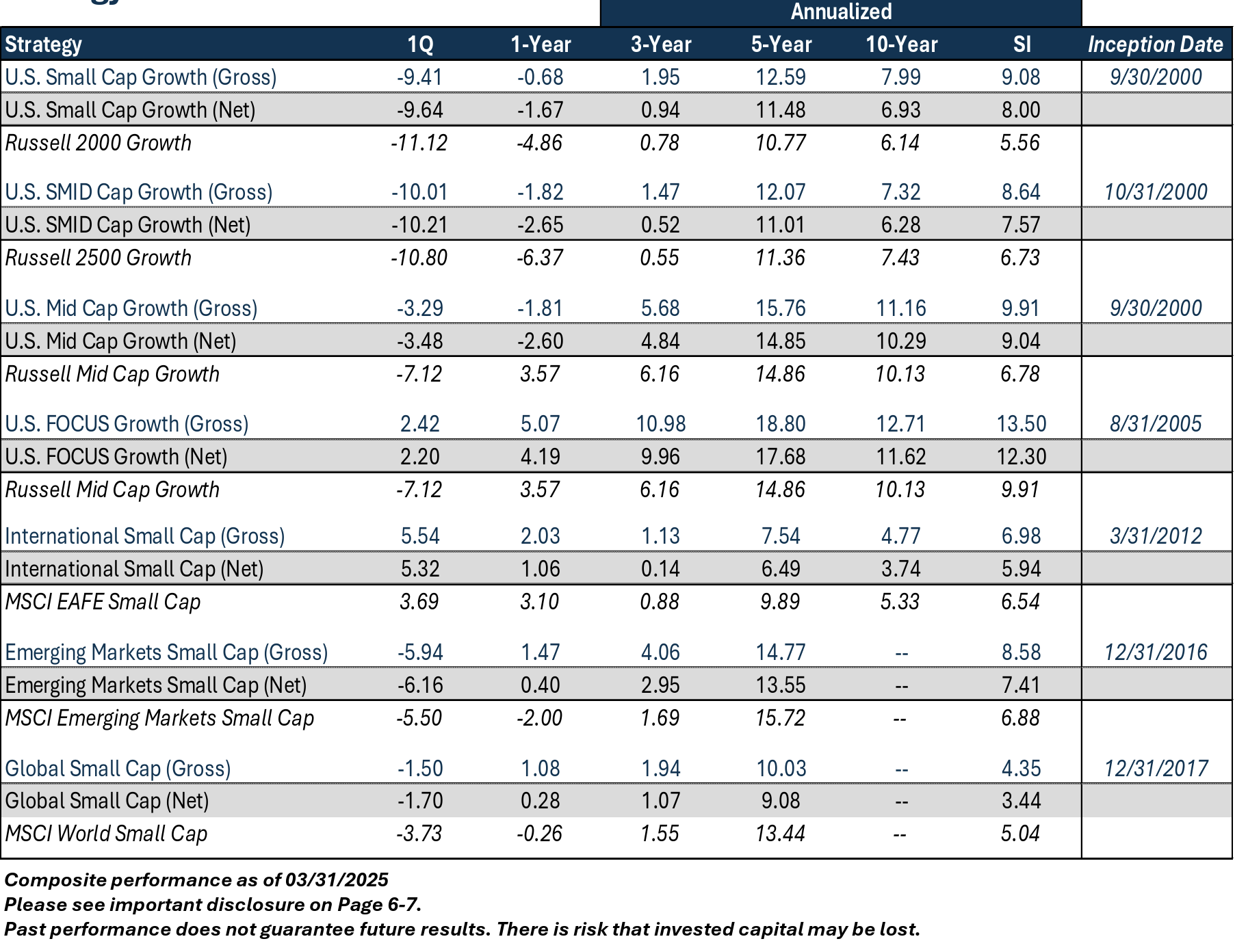

Strategy Performance

Updated Profiles & Commentaries Here

TimesSquare Recent Insights

Emerging Markets, With or Without China

Investing Beyond Borders: Weighing China’s impact amid economic and geopolitical shifts.

Beyond the Headlines

Navigating Semiconductor Cycles: Uncover how end-market exposure shapes the evaluation of semiconductor companies in a dynamic industry.

The Importance of Quality

Defining Quality in Investing: Explore how TimesSquare integrates quality in our investment approach.

The Next Chapter: Japan’s Quality Growth Story Unfolds

Exploring Japan’s Investment Landscape: Dive into our latest insights on how market dynamics are reshaping investment opportunities in Japan.

1 Source: Robert Shiller (https://shillerdata.com/), Price earnings ratio is based on average inflation-adjusted earnings from the previous 10 years, known as the Cyclically Adjusted PE Ratio (CAPE Ratio). Data from January 1,1871 to April 3, 2025.

2 Source: FactSet, MSCI, FY1 PE was used for this analysis. 3/31/2015-3/31/2025.

3 Source: FactSet, MSCI, 3/31/2025.

4 Source: FactSet, MSCI, TimesSquare Capital Management, LLC.

Disclosures

TimesSquare Capital Management LLC is a growth equity specialist that is registered as an investment adviser with the U.S. Securities and Exchange Commission and is majority owned by Affiliated Managers Group, Inc. With an experienced investment team and rigorous fundamental analysis, we identify high quality companies with strong management in inefficient market cap ranges. As a boutique, our highly collaborative process and integrated approach promote our commitment to meeting our clients’ service needs. Importantly, employees share a common economic interest through equity participation aligning them with the success of our clients and the firm.

This material is for your private information and is provided for educational purposes only. The views expressed are the views of TimesSquare Capital Management, LLC only through the period ended June 2025 and are subject to change based on market and other conditions. The opinions expressed may differ from those with different investment philosophies. The information we provide does not constitute investment advice and it should not be relied on as such. It should not be considered an offer or solicitation to buy or an offer to sell a security. It does not consider any investor’s particular investment objectives, strategies, tax status or investment horizon. We encourage you to consult your tax or financial advisor. All material has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy of, nor liability for, decisions based on such information. Specific investments described herein do not represent all investment decisions made by TimesSquare. No assumption should be made that investment decisions identified and discussed were or will be profitable. Specific investment advice references provided herein are for illustrative purposes only and are not necessarily representative of investments that will be made in the future.

TimesSquare Capital Management, LLC claims compliance with the Global Investment Performance Standards (GIPS®) and is independently verified. A firm that claims compliance with the GIPS standards must establish policies and procedures for complying with all the applicable requirements of the GIPS standards. Verification provides assurance on whether the firm's policies and procedures related to composite and pooled fund maintenance, as well as the calculation, presentation, and distribution of performance, have been designed in compliance with the GIPS standards and have been implemented on a firm-wide basis. Policies for valuing investments, calculating performance, and preparing GIPS Reports are available upon request. GIPS® is a registered trademark of CFA Institute. CFA Institute does not endorse or promote this organization, nor does it warrant the accuracy or quality of the content contained herein.

Certain information contained herein has been obtained from third party sources and such information has not been independently verified by TSCM. No representation, warranty, or undertaking, expressed or implied, is given to the accuracy or completeness of such information by TSCM or any other person. While such sources are believed to be reliable, TimesSquare does not assume any responsibility for the accuracy or completeness of such information. It does not undertake any obligation to update the information contained herein as of any future date.

Any indices and other financial benchmarks shown are provided for illustrative purposes only, are unmanaged, reflect reinvestment of income and dividends and do not reflect the impact of advisory fees. Investors cannot invest directly in an index. Comparisons to indexes have limitations because indexes have volatility and other material characteristics that may differ from a particular hedge fund. For example, a hedge fund may typically hold substantially fewer securities than are contained in an index.

Certain information contained herein constitutes “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results or actual performance may differ materially from those reflected or contemplated in such forward-looking statements. Nothing contained herein may be relied upon as a guarantee, promise, assurance or a representation as to the future.

U.S. Small Cap Growth: Performance is measured against the Russell 2000® Growth – a market capitalization-weighted index that measures the performance of those Russell 2000® companies with higher price-to-book ratios and higher forecasted growth rates. All indexes, including the Russell 2000® Growth Index, are based on gross-of-fee returns. FTSE Russell is the source and owner of the Russell Index data contained or reflected in this material and all trademarks and copyrights related thereto. Benchmark returns are not covered by the report of independent verifiers.

U.S. Small/Mid Cap Growth: Performance is measured against the Russell 2500 measures the performance of those Russell 2500 Growth – a market capitalization-weighted index that companies with higher price-to-book ratios and higher forecasted growth rates. All Growth Index, are based on gross-of-fee returns. FTSE Russell is the source and owner of the Russell indexes, including the Russell 2500 Index data contained or reflected in this material and all trademarks and copyrights related thereto. Benchmark returns are not covered by the report of independent verifiers.

U.S. Mid Cap Growth: Performance is measured against the Russell Midcap® Growth – a market capitalization-weighted index that measures the performance of those Russell Midcap® companies with higher price-to-book ratios and higher forecasted growth rates. All indexes, including the Russell Midcap® Growth Index, are based on gross-of-fee returns. FTSE Russell is the source and owner of the Russell Index data contained or reflected in this material and all trademarks and copyrights related thereto. Benchmark returns are not covered by the report of independent verifiers.

U.S. FOCUS Growth: Performance is measured against the Russell Midcap® Growth – a market capitalization-weighted index that measures the performance of those Russell Midcap® companies with higher price-to-book ratios and higher forecasted growth rates. All indexes, including the Russell Midcap® Growth Index, are based on gross-of-fee returns. FTSE Russell is the source and owner of the Russell Index data contained or reflected in this material and all trademarks and copyrights related thereto. Benchmark returns are not covered by the report of independent verifiers.

International Small Cap: Performance is measured against the MSCI EAFE Small Cap (Net) Index. MSCI EAFE Small Cap (Net) Index is a trade or service mark of MSCI Inc. The MSCI EAFE Small Cap (Net) Index is an unmanaged, market-weighted index of small companies in developed markets, excluding the U.S. and Canada. Its returns include net reinvested dividends but, unlike the Composite returns shown, do not reflect the payment of sales commissions or other expenses incurred in the purchase or sale of the securities included in the Index. All indexes, including the MSCI EAFE Small Cap (Net) Index, are based on gross-of-fee returns, including net reinvested dividends. Benchmark returns are not covered by the report of independent verifiers.

Global Small Cap: Performance is measured against the MSCI World Small Cap (Net) Index. MSCI World Small Cap (Net) Index is a trade or service mark of MSCI Inc. The MSCI World Small Cap (Net) Index is an unmanaged, market-weighted index of small companies in developed markets. Its returns include net reinvested dividends but, unlike the Composite returns shown, do not reflect the payment of sales commissions or other expenses incurred in the purchase or sale of the securities included in the Index. All indexes, including the MSCI World Small Cap (Net) Index, are based on gross-of-fee returns, including net reinvested dividends. Benchmark returns are not covered by the report of independent verifiers.

Past performance does not guarantee future results.

There is risk that invested capital may be lost. For more information, please contact us at info@tscmllc.com.

(Blue%20%26%20Gold)(Transparent)(2125x844)%20PNG.png)