Navigating Small Cap Biopharma

Health care, particularly biopharma, stands as one of the most dynamically innovative sectors in the global economy, serving as a beacon of scientific advancement that continuously reshapes the landscape of medical treatment and patient care.

David Ferreiro, Ph.D., Portfolio Manager

Health care, particularly biopharma, stands as one of the most dynamically innovative sectors in the global economy, serving as a beacon of scientific advancement that continuously reshapes the landscape of medical treatment and patient care. Since the groundbreaking Human Genome Project published its first working draft in 2000 and achieved its monumental completion in 2003, we have witnessed an extraordinary acceleration in biopharma innovation that has fundamentally transformed the practice of medicine.

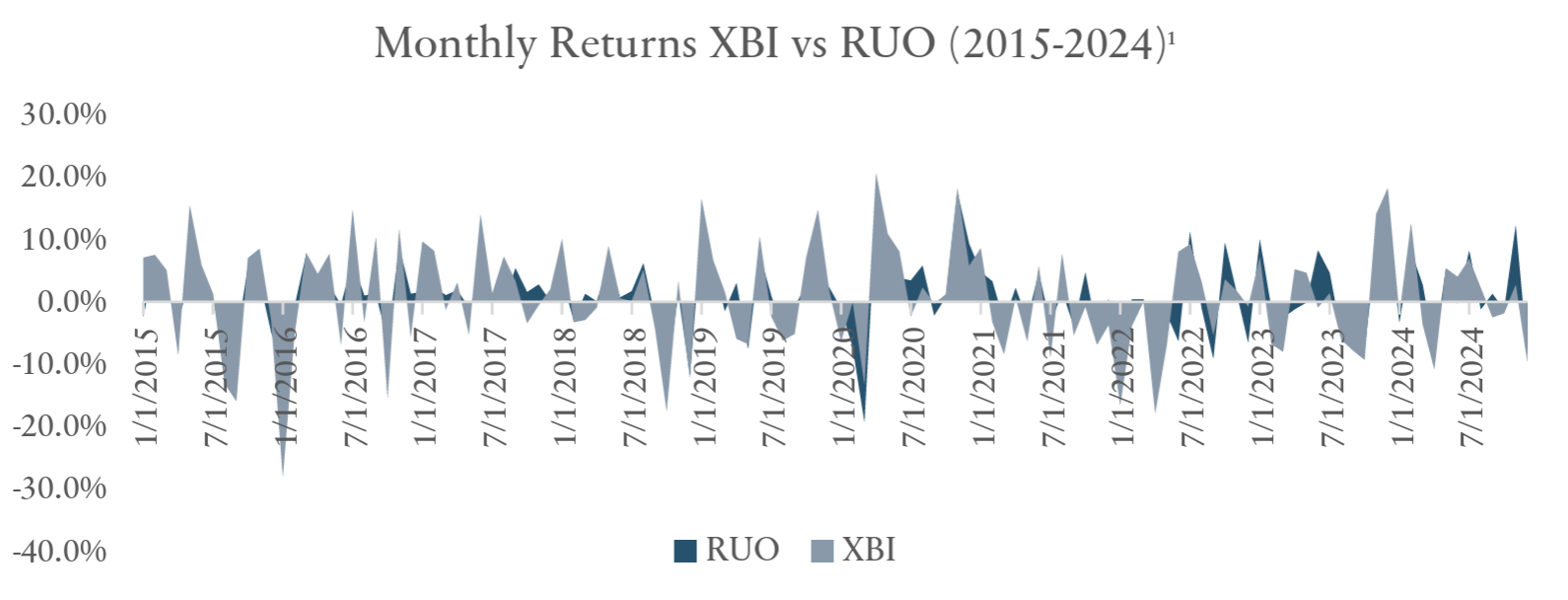

Investors are historically wary of small cap biopharma given the need for technical knowledge and the potential for high volatility, concerns that are certainly validated by market data. As illustrated in the accompanying chart1 showing monthly returns from 2015-2024, the XBI index (an equal-weighted S&P biotech ETF) demonstrates significantly higher volatility compared to the Russell 2000® Growth Index (RUO), with annualized volatility of 29.55% versus 21.16% respectively. This 40% higher volatility in XBI is statistically significant and highlights the notable risk that many investors face. Since XBI is an equalweighted index that includes larger cap biotech companies, small cap biotech investments would be expected to exhibit even greater volatility than these already elevated levels. This combination of technical complexity in evaluating drug development pipelines, regulatory risks, and the extreme price volatility evident in the data explains why many investors approach the sector with considerable caution, despite its potential for outsized returns during favorable periods.

The Small Cap Opportunity in Biopharma

Despite the inherent risks and volatility that characterize small cap biopharma investments, several compelling structural factors make the industry increasingly attractive for long-term investors. The convergence of powerful demographic tailwinds, including a rapidly aging population and rising obesity epidemic, coupled with health care expenditures consistently outpacing GDP growth, creates sustained demand for innovative therapeutic solutions that biopharma companies are uniquely positioned to deliver.

Furthermore, the high cost of drug development, long regulated development processes, highly regulated supply chains, and intellectual property patent protection provide significant barriers to entry. In addition, novel green field market opportunities such as first-in-class therapies in new disease markets enjoy substantial and quantifiable advantages that create lasting competitive moats. Over the last 5 years, small cap biopharma has been a primary source of innovation with ~65% market share² for new drug launches.

Our Approach to Investing in Small Cap Biopharma

As quality growth managers, we employ a rigorous investment process that has been refined over the past 20 years. It focuses on three core pillars for identifying companies: distinct, sustainable competitive advantages, quality management teams, and strong consistent growth profiles. Within the small cap biopharma universe, where the developmental, high-risk, and cash-burning nature of these companies scares many fundamental growth managers away from the sub-sector, we have applied a rigid investment process to find companies that fit our investment criteria. This process centers on identifying companies developing first-in-class therapeutics that represent true greenfield opportunities in areas of significant unmet medical needs. We look for rare disease opportunities and targeted therapeutics that address specific patient populations with precision, and novel drug targets in large disease areas where traditional approaches have failed. We place particular emphasis on management quality given the complex developmental pathways and regulatory interactions inherent in drug development, recognizing that successful drug approval requires exceptional leadership with a clear vision for navigating the intricate regulatory landscape from preclinical studies through clinical trials to FDA approval.

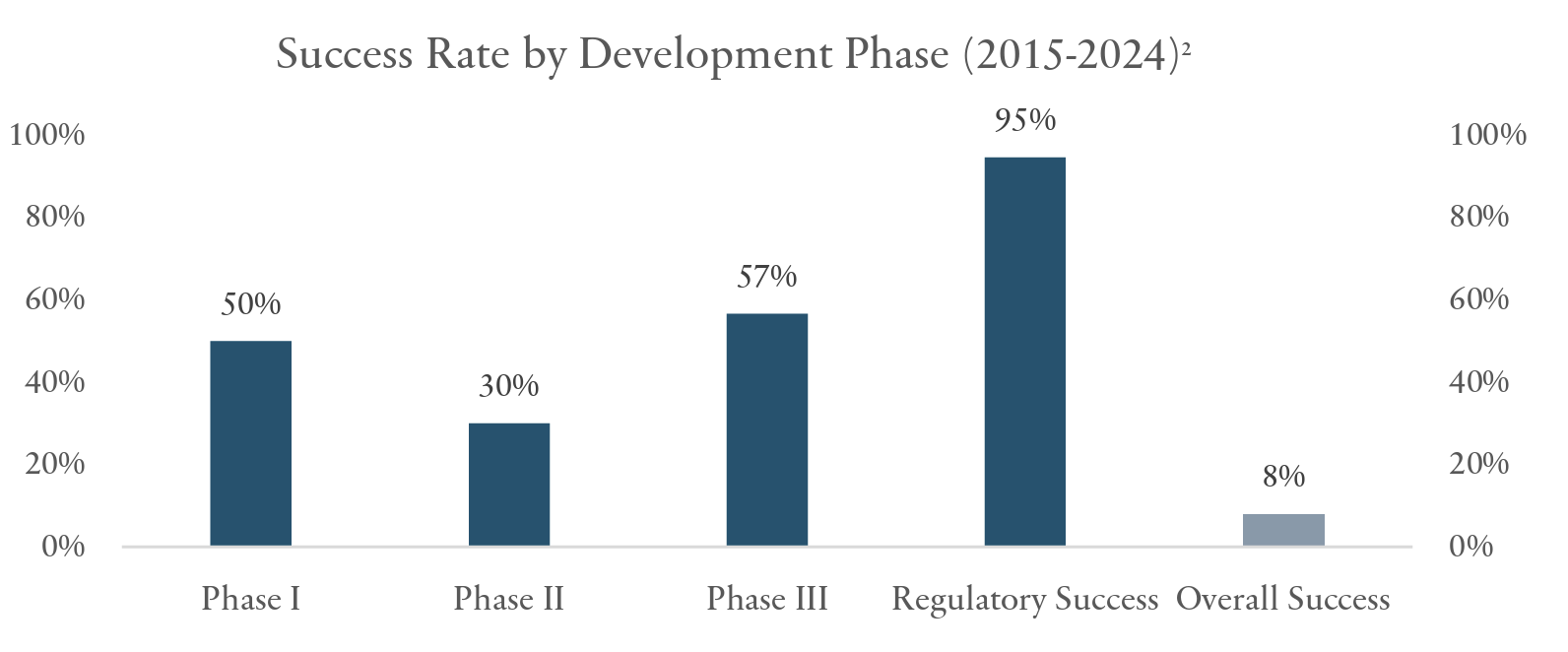

Small cap biopharma investing presents a distinctive risk-reward proposition shaped by the inherently challenging nature of drug development, where the overall success rate2 from initial discovery to market approval hovers around just 8%. We focus our attention on companies that have successfully navigated past the proof-of-concept stage, particularly those with Phase II data in hand. Phase II represents the most critical inflection point in drug development, where success rates2 plummet to just 30% thereby supporting our strategic approach. By concentrating on post-Phase II opportunities, we can avoid the highest attrition phase while still capturing significant upside potential, as companies with validated proof-of-concept data face substantially improved odds of 57% and 95% success rates2 in Phase III and regulatory approval, respectively.

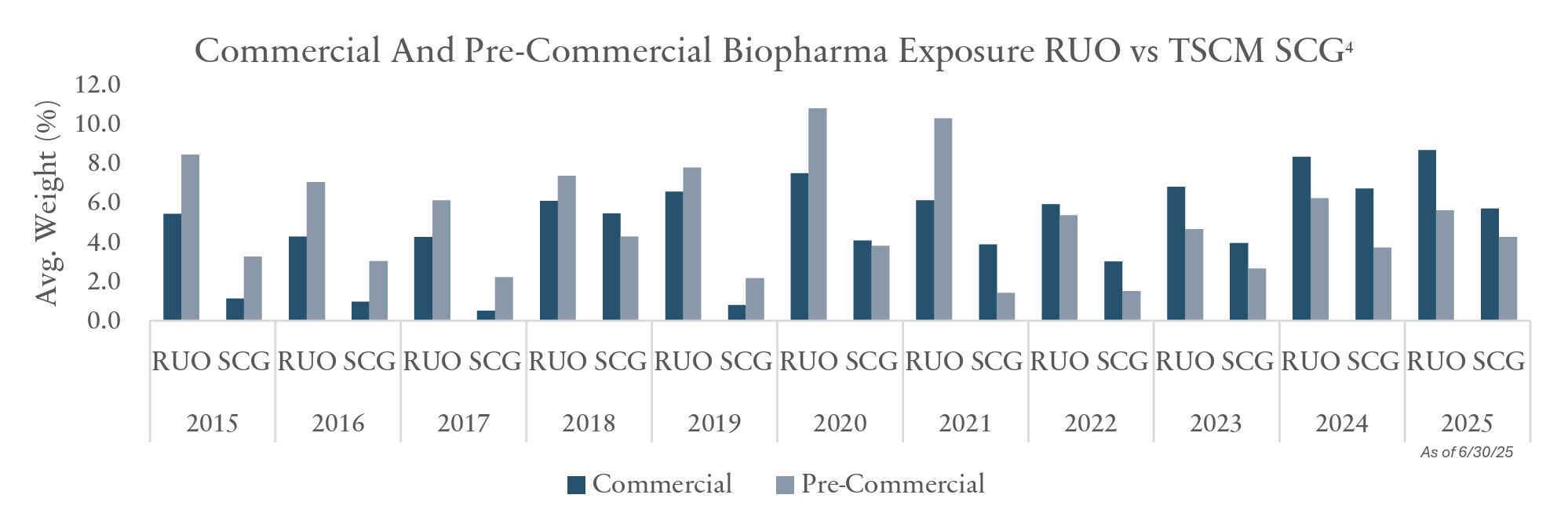

As quality growth managers we have maintained a consistent underweight to biopharma, due in part to our intentional avoidance of some of the more speculative early stage, pre-commercial biopharma companies that populate the index and possess significant levels of binary risk. Thus, we strategically tilt our portfolio weighting3 to commercial companies and maintain a more pronounced underweight to pre-commercial biopharma (~-400bps) vs commercial biopharma (~-300bps).

We believe our strategic approach to biopharma investing has been successful, generating substantial alpha in a risk disciplined manner while maintaining significant underweight relative to the benchmark. From 2015 through June 2025, our biopharma positioning4 contributed 107 bps of annualized gross outperformance, while maintaining an average underweight of approximately 680 bps. We believe this performance demonstrates the effectiveness of our selective stock-picking approach, focusing on quality companies with strong fundamentals rather than simply matching benchmark weights or taking a basket approach. Additionally, our strategy5 has benefited from persistent merger and acquisition activity within the sector, as approximately 15% of our unique biopharma investments have been acquired by larger companies, providing a meaningful tailwind to our returns. This M&A activity validates our ability to identify attractive takeover targets and underscores the value creation potential inherent in our carefully curated biopharma holdings, further contributing to consistent outperformance despite an underweight positioning.

This insight paper serves as just a glimpse into the longer-form and highly detailed Navigating Small Cap Biopharma white paper that we are pleased to provide upon request.

1 Source: Bloomberg, RUO, XBI.

2 Source: IQVIA Institute, Global Trends in R&D 2025, March 2025.

3 Source: TimesSquare Capital Management, LLC, as of 6/30/25.

4 Source: FactSet, RUO, TimesSquare Capital Management, LLC.

5 Source: TimesSquare Capital Management, LLC. The use of logos mentioned does not imply endorsement by the presenter.

This material is for your private information and is provided for educational purposes only. The views expressed are the views of TimesSquare Capital Management, LLC only through the period ending June 2025 and are subject to change based on market and other conditions. The opinions expressed may differ from those with different investment philosophies. The information we provide does not constitute investment advice and it should not be relied on as such. It should not be considered an offer or solicitation to buy or an offer to sell a security. It does not consider any investor’s particular investment objectives, strategies, tax status or investment horizon. We encourage you to consult your tax or financial advisor. All material has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy of, nor liability for, decisions based on such information. Specific investments described herein do not represent all investment decisions made by TimesSquare. No assumption should be made that investment decisions identified and discussed were or will be profitable. Specific investment advice references provided herein are for illustrative purposes only and are not necessarily representative of investments that will be made in the future.

TimesSquare Capital Management LLC is a growth equity specialist that is registered as an investment adviser with the U.S. Securities and Exchange Commission and is majority owned by Affiliated Managers Group, Inc. With an experienced investment team and rigorous fundamental analysis, we identify high quality companies with strong management in inefficient market cap ranges. As a boutique, our highly collaborative process and integrated approach promote our commitment to meeting our clients’ service needs. Importantly, employees share a common economic interest through equity participation, aligning them with the success of our clients and the firm.

TimesSquare Capital Management, LLC

75 Rockefeller Plaza, 30th Floor, New York, NY 10019

©Copyright 2025 TimesSquare Capital Management, LLC. All rights reserved.

This document may not be reproduced, in whole or in part, without permission of the author.

(Blue%20%26%20Gold)(Transparent)(2125x844)%20PNG.png)