The Chip Game: Beyond the Headlines

The semiconductor industry is broadly recognized as one that periodically undergoes a boom-bust cycle.

Jason Shum, CFA and Leona Yang, CFA

The semiconductor industry is broadly recognized as one that periodically undergoes a boom-bust cycle. This group encompasses not only manufacturers of chips and related components, but also testing companies as well as those that supply manufacturing equipment and services to the industry. Due to its interdependent ecosystem and the vast array of end markets served, the semiconductor industry is incredibly diverse and complex.

By now, the constant appearance of AI in headlines has continually reminded investors of the surging demand for chips. Riding this supercycle, companies with exposure to data centers or perceived ties to AI (e.g., Nvidia, Fabrinet, Supermicro) have enjoyed outsized price returns.

However, the performance of individual semiconductor companies has varied. Because the industry is tied to various end markets at different stages of recovery, we believe there are still significant investment opportunities beyond the current focus of headlines. Many semiconductor companies supply multiple end markets, and it is important to dissect their exposures and understand their position within the respective cycle.

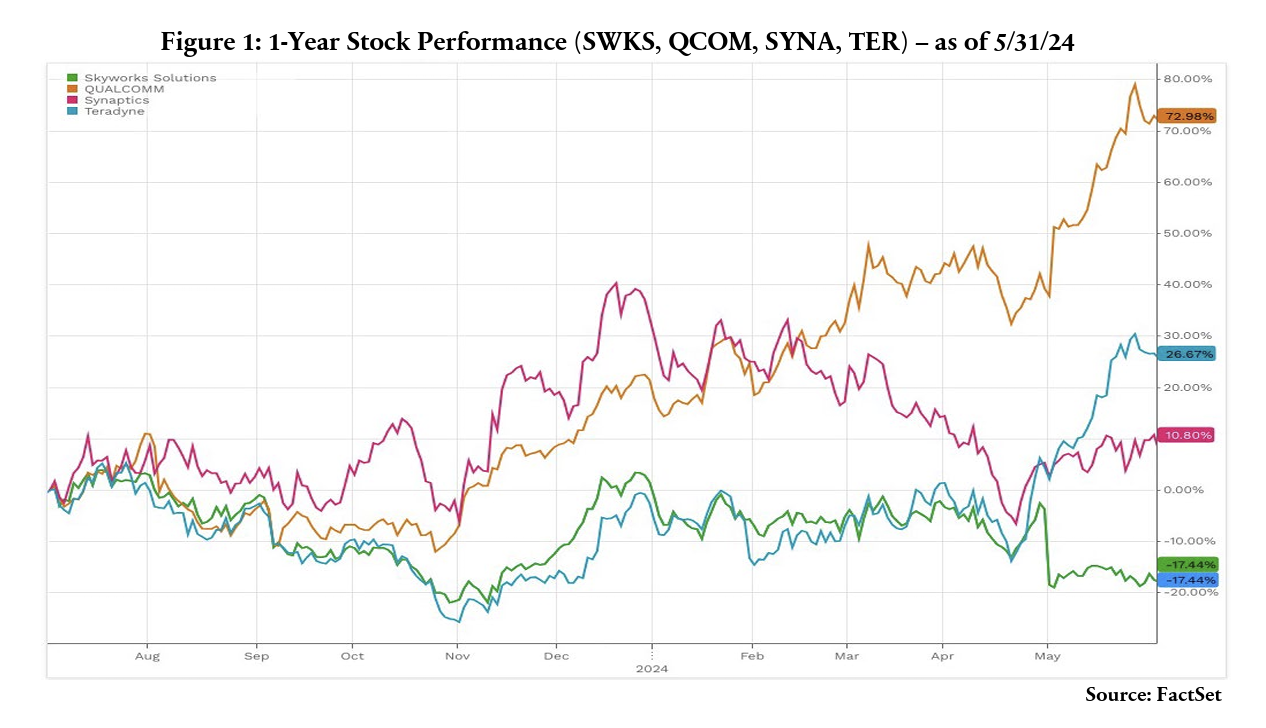

Smartphones and PCs – Entering Recovery

The smartphone market was the first to enter a downturn in 2022. In the third quarter of 2023, we started seeing green shoots, and in the fourth quarter of 2023, the 8% year-on-year growth1 (especially from strength in the Android market) further demonstrated stabilization and recovery. There is a similar story in the global PC market, which returned to growth in the first quarter of 2024 after two years of decline2 according to the International Data Corporation (IDC).

In this segment, while most of the companies troughed in either the third or fourth quarter of 2023, there were divergences in performance. Companies such as Skyworks (heavily tied to the iPhone market) and Synaptics (more exposed to enterprise PCs) have seen much bumpier roads to recovery. Meanwhile, companies including QUALCOMM and Teradyne (on the testing side), with more broad-based end market exposures, are experiencing tailwinds as specific areas see improvements.

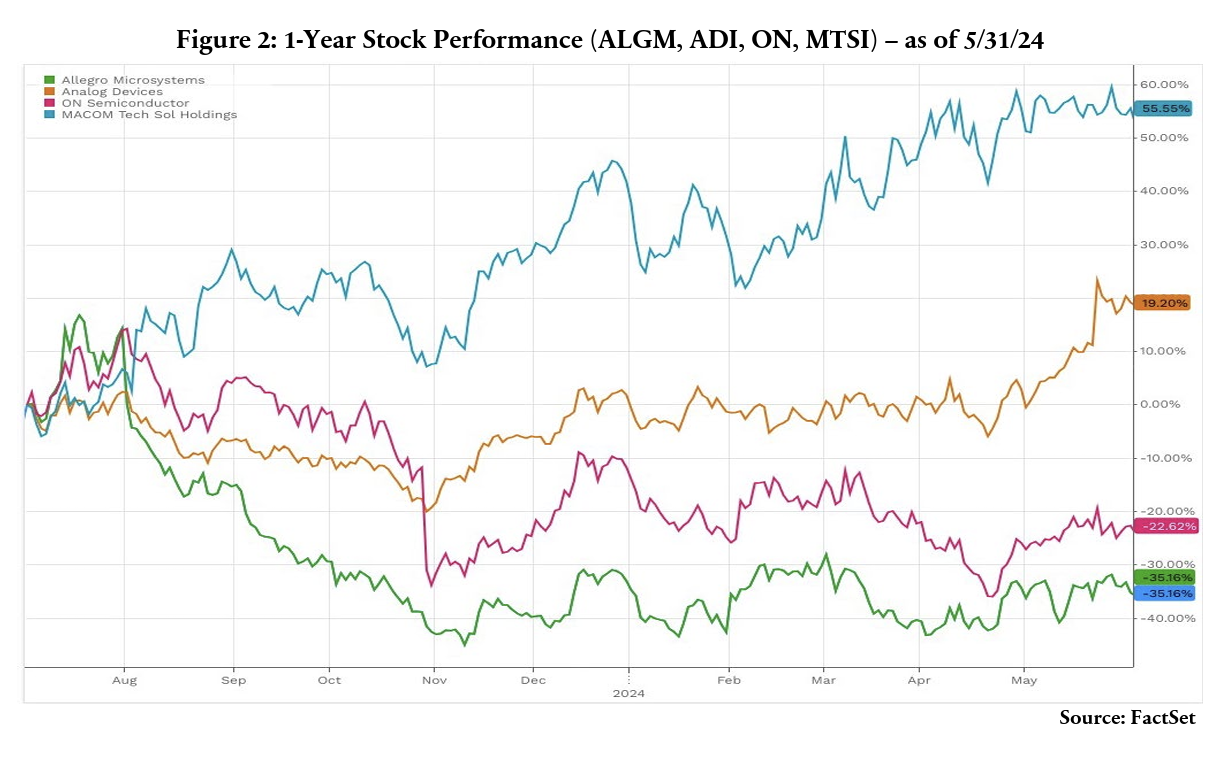

Industrial and Automotive – Treading Water

Industrial was the next to fall. Within this broad sector, aerospace and defense companies generally fared better, and so did chip companies that are exposed to this segment (e.g. MACOM Tech Solutions). As the automotive industry continued its downward trend, suppliers to this end market have been hesitant to call for a quick recovery but expect stabilization along the bottom with potential for recovery later in 2024 (i.e. ON Semiconductor and Allegro Microsystems). Meanwhile, we are seeing early signs of cyclical recovery in the analog space. In fact, Analog Devices was one of the first suppliers to call out a turnaround, with bookings continuing to improve.

Telecommunications – Bottoming Out

Telecommunications was one of the earlier end markets that fell as wireless carriers scaled back on 5G and broadband spending (partly due to higher interest rates). Though a recovery has yet to start, there are early signs suggesting that we are approaching the bottom. Many of the companies that are heavily exposed to the telecommunications industry are telecom equipment producers, with a subset that also produce Silicon Carbide (SiC) wafers (e.g. Coherent). For these companies (as illustrated in the chart below), they still have a long road to recovery.

Conclusion

End market exposure is a key consideration when evaluating semiconductor companies. As such, it is important to carefully comb through the noise and truly understand how different semiconductor companies fit into the current cycle

1 Canalys research: https://www.canalys.com/newsroom/worldwide-smartphone-market-2023

2 IDC Research: https://www.idc.com/getdoc.jsp?containerId=prUS52019024

TimesSquare Capital Management LLC is a growth equity specialist that is registered as an investment adviser with the U.S. Securities and Exchange Commission and is majority owned by Affiliated Managers Group, Inc. With an experienced investment team and rigorous fundamental analysis, we identify high quality companies with strong management in inefficient market cap ranges. As a boutique, our highly collaborative process and integrated approach promote our commitment to meeting our clients’ service needs. Importantly, employees share a common economic interest through equity participation aligning them with the success of our clients and the firm.

This material is for your private information and is provided for educational purposes only. The views expressed are the views of TimesSquare Capital Management, LLC only through the period ended May 2024 and are subject to change based on market and other conditions. The opinions expressed may differ from those with different investment philosophies. The information we provide does not constitute investment advice and it should not be relied on as such. It should not be considered an offer or solicitation to buy or an offer to sell a security. It does not consider any investor’s particular investment objectives, strategies, tax status or investment horizon. We encourage you to consult your tax or financial advisor. All material has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy of, nor liability for, decisions based on such information.

TimesSquare Capital Management, LLC

75 Rockefeller Plaza, 30th Floor, New York, NY 10019

©Copyright 2024 TimesSquare Capital Management, LLC. All rights reserved.

This document may not be reproduced, in whole or in part, without permission of the author.

(Blue%20%26%20Gold)(Transparent)(2125x844)%20PNG.png)