The Next Chapter: Japan’s Quality Growth Story Unfolds

Exploring Japan’s Investment Landscape: Dive into our latest insights on how market dynamics are reshaping investment opportunities in Japan.

How Tokyo Stock Exchange’s “Letter of Shame” is reshaping the investment landscape in Japan

Portfolio Manager

Portfolio Manager

CFA Product Manager

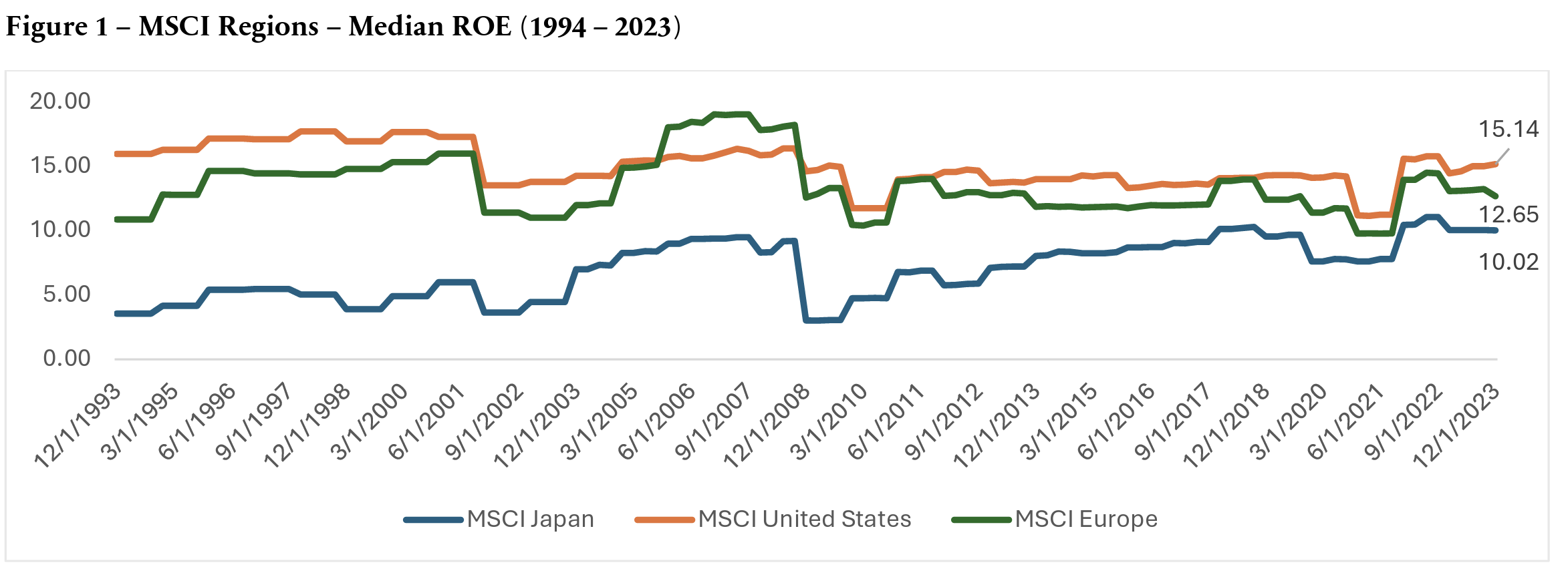

Following the collapse of Japan’s asset price bubble in the 1990s, the Japanese equity market largely mirrored the country’s “lost decades.” On top of the sluggishness in the market, Japanese companies were not shareholder friendly, which further pushed foreign investors away from the market. While companies took some steps to move towards more Western-style corporate governance, they still did not truly prioritize shareholder interests. As evident in the chart below, the median Return on Equity (ROE) of Japanese equities lagged both the US and Europe over the last 30 years.

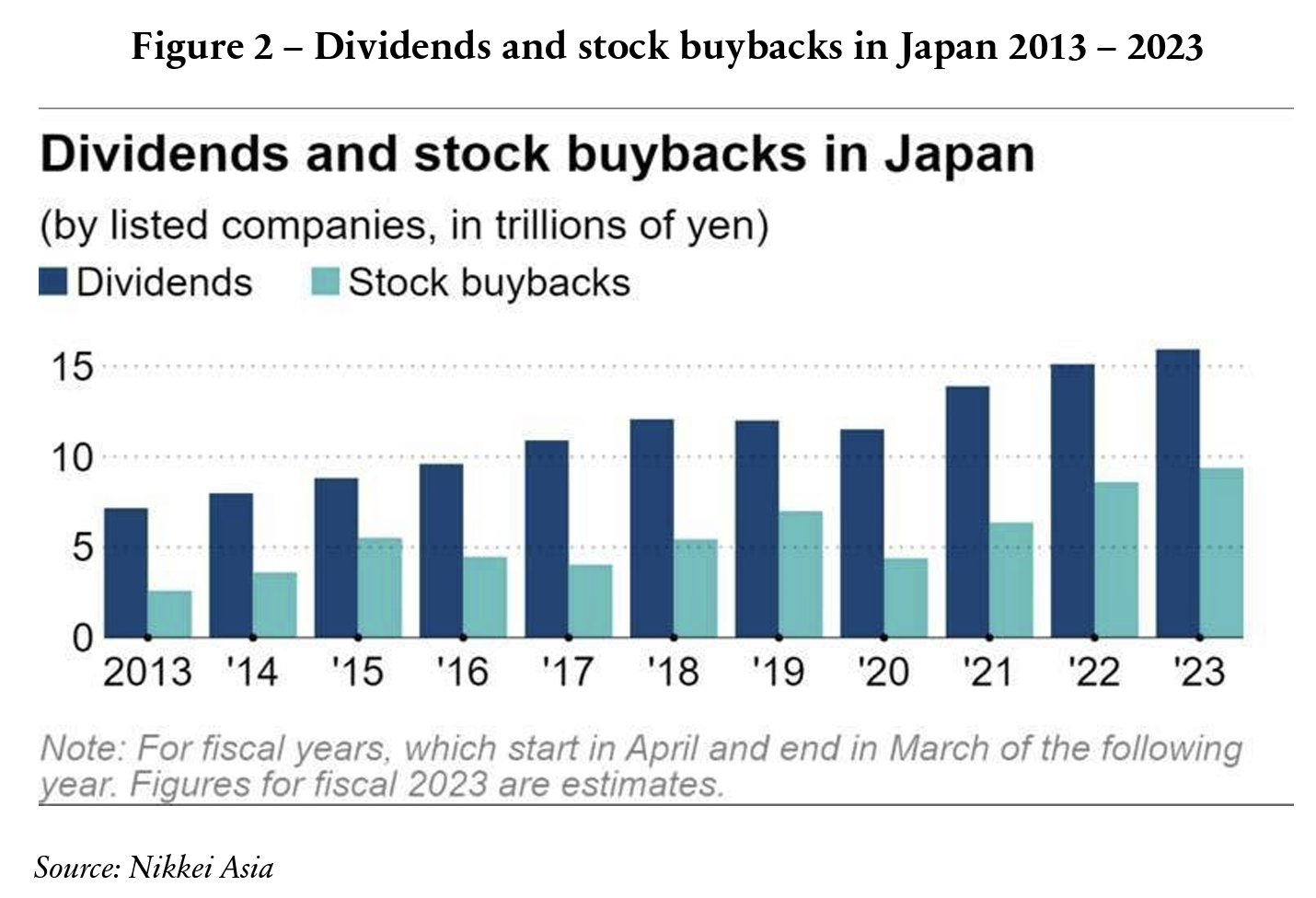

However, in 2023 the Tokyo Stock Exchange issued a letter to its listed companies, urging them to pay more attention to capital costs and stock prices1. The exchange adopted a radical “named and shamed” strategy towards companies trading below book value and required them to disclose concrete plans to improve their capital efficiency and lift stock prices1. Armed with this “letter of shame”, activist investors turned to deep Value companies and intensified their pressure on them. Throughout 2023, many share buybacks were announced, which totaled to a record $65 billion for the full year2. Total payouts to shareholders through dividends and stock buybacks are expected to reach an all-time high of about 25 trillion yen ($165 billion) for the fiscal year ending March 20243.

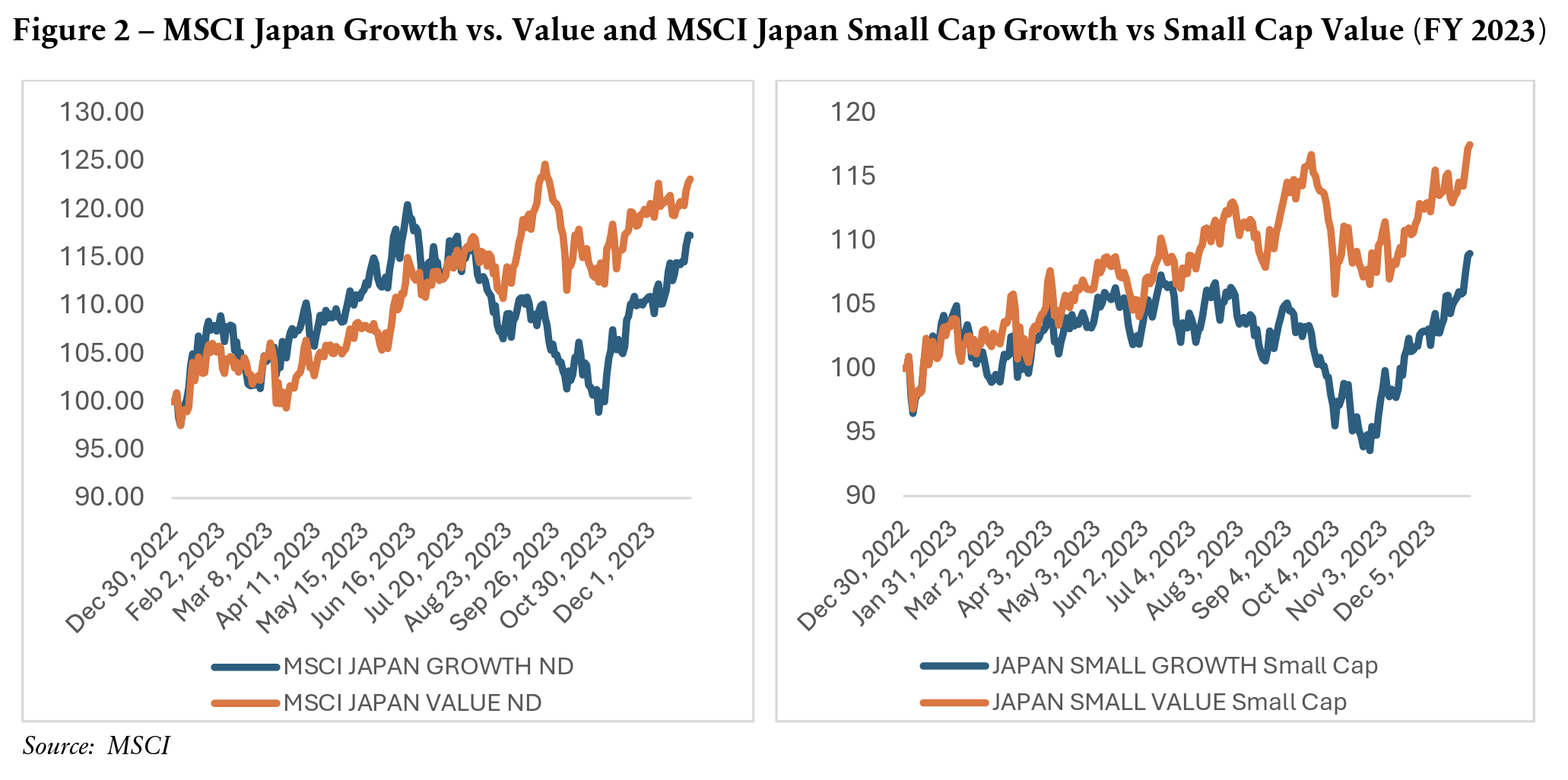

This was great news for Value investors; in fact, Japanese Value stocks outperformed their Growth peers by 5.8% in 2023. Within Japanese small caps, where we focus our attention, the spread between Value and Growth was even more pronounced, with MSCI Japan Small Cap Value outperforming Small Cap Growth by 8.5%.

While Japan’s rotation to Value was a headwind for quality growth managers like us in 2023, this significant shift has started to normalize. Going forward, we believe TSE’s “letter of shame” creates a multi-year runway for quality growth investing in Japan for the following reasons:

- The emphasis on capital efficiency and share prices steers companies to improve profitability and shareholder value. While short-term gains in shareholder value might be achieved through improved capital efficiency for even lower-quality companies, sustainable growth in ROE comes from high-quality businesses. These companies achieve this by "climbing the value chain" through reinvestment in R&D and other initiatives that drive future growth.

- Through share buybacks and dividends, capital was put back into the Japanese economy and we see signs of that capital getting redeployed to propel future growth.

- The shift to a more shareholder friendly mindset and corporate governance reform could serve as a catalyst to attract foreign investors who have long underweighted the Japanese market.

Contrary to the U.S., where indices are dominated by fast growing areas of the market, Japan’s indices are heavily exposed to cyclical and low growth areas. To access Japan’s unique growth opportunities, it requires deep fundamental research to uncover structural growers that are well-managed, provide differentiated products and or services, and carry sustainable competitive advantages. We believe these high-quality companies offer compelling long-term growth prospects, and TSE’s focus on shareholder value will provide an additional boost.

“Letter of Shame” (available in PDF form upon request).

1 “Tokyo bourse tells Toyota, SoftBank, others to lift capital efficiency”, Nikkei Asia, April 1, 2023 (available in PDF form upon request).

2 “Japan firms’ share buybacks expanded to a record $65bn in 2023”, Nikkei Asia, January 30, 2024 (available in PDF form upon request).

3 “Japan Inc. to return record $165bn to shareholders as profits rise”, Nikkei Asia, March 26, 2024 (available in PDF form upon request).

TimesSquare Capital Management LLC is a growth equity specialist that is registered as an investment adviser with the U.S. Securities and Exchange Commission and is majority owned by Affiliated Managers Group, Inc. With an experienced investment team and rigorous fundamental analysis, we identify high quality companies with strong management in inefficient market cap ranges. As a boutique, our highly collaborative process and integrated approach promote our commitment to meeting our clients’ service needs. Importantly, employees share a common economic interest through equity participation aligning them with the success of our clients and the firm.

This material is for your private information and is provided for educational purposes only. The views expressed are the views of TimesSquare Capital Management, LLC only through the period ended February 2024 and are subject to change based on market and other conditions. The opinions expressed may differ from those with different investment philosophies. The information we provide does not constitute investment advice and it should not be relied on as such. It should not be considered an offer or solicitation to buy or an offer to sell a security. It does not consider any investor’s particular investment objectives, strategies, tax status or investment horizon. We encourage you to consult your tax or financial advisor. All material has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy of, nor liability for, decisions based on such information.

TimesSquare Capital Management, LLC 7

5 Rockefeller Plaza, 30th Floor, New York, NY 10019

©Copyright 2024 TimesSquare Capital Management, LLC. All rights reserved.

This document may not be reproduced, in whole or in part, without permission of the author.

(Blue%20%26%20Gold)(Transparent)(2125x844)%20PNG.png)