Why International and Why Now

Investors have favored the U.S. equity market for many years. However, with U.S. stocks currently experiencing historically high valuations and an uncertain economic outlook, there is a growing interest to look beyond the domestic markets.

Magnus Larsson, David Hirsh and Leona Yang, CFA

Investors have favored the U.S. equity market for many years. However, with U.S. stocks currently experiencing historically high valuations and an uncertain economic outlook, there is a growing interest to look beyond the domestic markets. We note in the following charts the historically high valuations in the U.S. equity market and the widening of that valuation gap versus other major world markets.

Case Studies – Europe and Japan

As a bottom-up quality growth specialist with decades of experience in international markets, we believe there are compelling opportunities outside the U.S. Below we examine Europe and Japan, the two largest markets within the ex-U.S. universe.

Europe

A growing awareness across Europe underscores the necessity of decoupling from foreign influences in various sectors. Beyond energy and, more recently, defense independence, current tariff concerns are highlighting the urgency of trade decoupling. Looking ahead, we anticipate a medium-term objective of greater European technological sovereignty, recognizing infrastructure like the cloud as strategic assets. This multifaceted decoupling trend will necessitate significant investment, which in turn will lead to growth within several key sectors of the European economy. Despite short-term headwinds causing lower business and consumer sentiment in Europe, increased reshoring and investments in domestic production provide an attractive backdrop. Furthermore, the historic German stimulus announced in March is the strongest evidence that the EU is up to the challenge and shouldn’t be underestimated in realizing this potential. For this medium-term expansion to materialize, Europe needs updated infrastructure, requiring government spending and lower taxes. The ongoing decline in Eurozone inflation also supports this positive outlook, allowing the European Central Bank to maintain an accommodative policy stance. Consequently, European economic growth should be buoyant in 2026. In the short term, this uncertainty might help the ECB manage inflation. Our approach in the region includes balanced exposure to both local structural growth drivers and global niche dominators.

Japan

After decades of stagnation, Japan is undergoing economic reforms, particularly in terms of corporate governance, labor market participation, and foreign investment. These changes should yield long-term growth.

The demographic reality of an aging population in Japan underscores the urgent need for advancements in technological innovation. To offset potential labor shortages and maintain productivity, the nation is increasingly focused on digitization across various sectors. This is expected to drive significant digital investment, coupled with the strategic implementation of AI to improve efficiency in industries ranging from manufacturing to services. Against this backdrop, companies that are involved in the development of local data centers, semiconductor foundries, or part of the electric grid ecosystems are poised for substantial long-term growth.

The major expansion of NISA (Nippon Individual Savings Account) in 2024 introduced changes to the system including making the NISA system permanent, the NISA tax-exempt holding period indefinite, and increasing the investment limits. Meanwhile, Japan’s corporate governance reform pushes Japanese companies to improve profitability and to drive future growth. These changes provide a supportive backdrop to Japanese equities.

With tariff worries weighing on export related sectors across the world, our attention is drawn to Japan’s robust inbound tourism. While closely monitoring this influx of international visitors, we also anticipate that the recent significant wage increases within Japan will provide a strong tailwind for domestic spending in the quarters ahead.

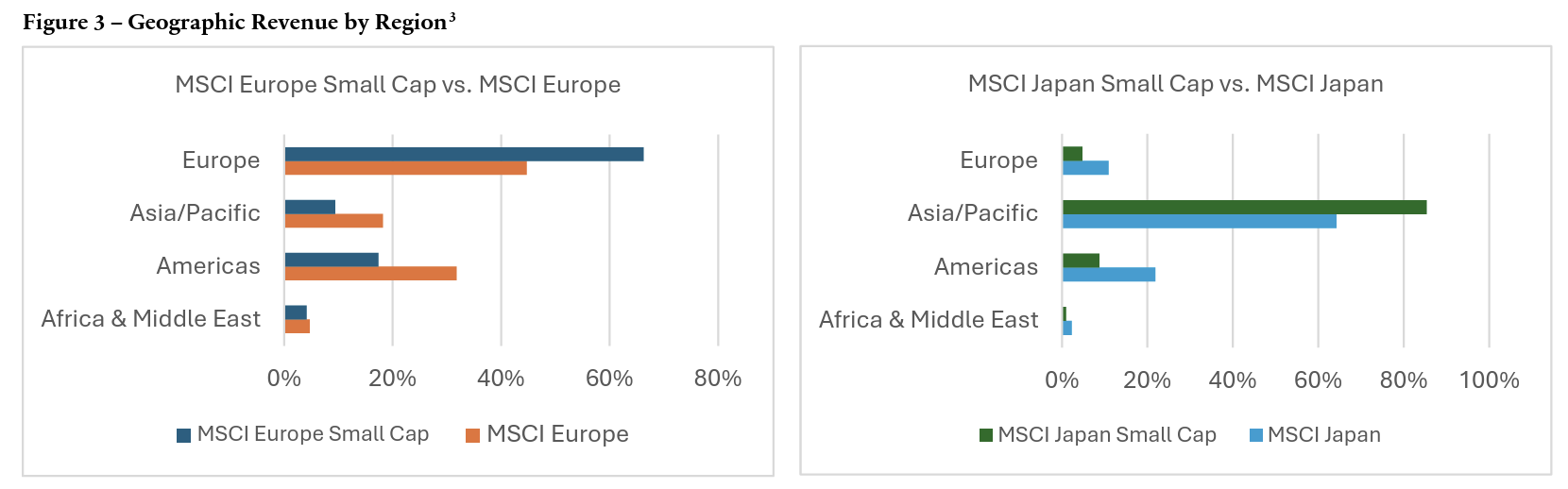

Small Caps

As illustrated in Figure 3, on average, smaller cap companies in Japan and Europe generate higher proportions of their revenues domestically. This ties them more directly to the local economic fundamentals and consumer behaviors. By allocating to small cap companies, investors have the opportunity to gain targeted exposure to local economies and potentially capture idiosyncratic growth opportunities that are less susceptible to global macroeconomic and geopolitical influences.

Why a Quality Growth approach matters?

Second Quarter 2025 Investment styles and asset classes may rise and fall in popularity during market cycles due to macroeconomic changes or investment sentiment. As bottom-up investors with a focus on business fundamentals, we seek high quality growth companies with a competitive edge - those with pricing power, strong management teams, and robust balance sheets. These companies, even during turbulent markets, tend to exhibit greater resilience and offer higher visibility in future growth. Given our preference for differentiated companies, we seek to have a positive exposure to profitability and growth highlighting an unwavering commitment to style consistency in our portfolio.

We believe the solidity of this approach will lead to better outcomes for our investors and do so in a risk-managed way.

1 Source: Robert Shiller (https://shillerdata.com/), Price earnings ratio is based on average inflation-adjusted earnings from the previous 10 years, known as the Cyclically Adjusted PE Ratio (CAPE Ratio). Data from January 1,1871 to April 3, 2025.

2 Source: FactSet, MSCI, FY1 PE was used for this analysis. 3/31/2015-3/31/2025.

3 Source: FactSet, MSCI, 3/31/2025.

4 Source: FactSet, MSCI, TimesSquare Capital Management, LLC.

This material is for your private information and is provided for educational purposes only. The views expressed are the views of TimesSquare Capital Management, LLC only through the period ending March 2025 and are subject to change based on market and other conditions. The opinions expressed may differ from those with different investment philosophies. The information we provide does not constitute investment advice and it should not be relied on as such. It should not be considered an offer or solicitation to buy or an offer to sell a security. It does not consider any investor’s particular investment objectives, strategies, tax status or investment horizon. We encourage you to consult your tax or financial advisor. All material has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy of, nor liability for, decisions based on such information.

TimesSquare Capital Management LLC is a growth equity specialist that is registered as an investment adviser with the U.S. Securities and Exchange Commission and is majority owned by Affiliated Managers Group, Inc. With an experienced investment team and rigorous fundamental analysis, we identify high quality companies with strong management in inefficient market cap ranges. As a boutique, our highly collaborative process and integrated approach promote our commitment to meeting our clients’ service needs. Importantly, employees share a common economic interest through equity participation, aligning them with the success of our clients and the firm.

TimesSquare Capital Management, LLC

75 Rockefeller Plaza, 30th Floor, New York, NY 10019

©Copyright 2025 TimesSquare Capital Management, LLC. All rights reserved.

This document may not be reproduced, in whole or in part, without permission of the author.

(Blue%20%26%20Gold)(Transparent)(2125x844)%20PNG.png)